6 Best Crypto Exchanges in South Korea

South Korea is one of the most active retail crypto markets on earth, and one of the most tightly controlled. The licensed domestic exchanges offer real-name account deals with a single Korean bank and accept won directly. Unfortunately, they are spot-only: no futures, margin, or leverage.

The global platforms, led by KuCoin, carry diverse asset lists and derivatives that Korean law bars local exchanges from offering. The downside is that there is no coverage under the Virtual Asset User Protection Act, and the mobile apps were removed from the Apple and Google Play Store.

So we funded each platform the way a Seoul resident would: won through real-name accounts on the domestic venues, P2P on the global ones, then traded BTC and ETH and withdrew funds. Here are the six best crypto exchanges for Korean investors:

Our Top Picks: Best Platforms for 2026

Top Crypto Exchange in Korea - KuCoin

KuCoin is the best crypto exchange in Korea as it provides free KRW deposits, low fees, a wide range of cryptocurrencies, unique features and the platform can be used in Korean.

Available Markets

1,000+ Cryptocurrencies

Trading Fees

0.1% Spot Trading Fee

KRW Deposit Methods

Cards, Apple Pay, P2P

Compare Top South Korean Crypto Exchanges

1. KuCoin

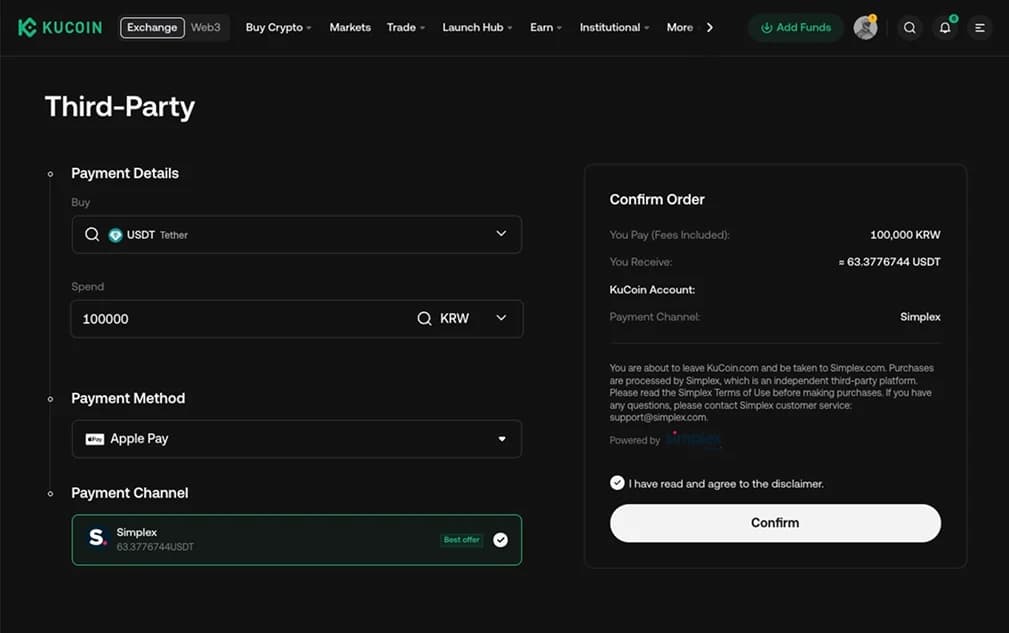

KuCoin tops the list for Koreans who want more than spot. It lists 900+ assets and runs Earn products, futures, margin, and trading bots at 0.10% spot fees, a range no licensed Korean exchange can match given the domestic ban on derivatives.

Access is the problem. KuCoin doesn’t support KRW bank transfers, so Koreans fund it by buying USDT through Apple Pay, credit/debit card or P2P, and its app was pulled from Korean stores in 2025 as an unregistered operator. You can only access it through a desktop or mobile browser.

It is not FIU-registered, so trades fall outside the Virtual Asset User Protection Act with no local recourse. The upside is the range of features that regional platforms cannot offer, including spot & futures trading, staking, crypto loans, trading bots, the KuCard, and an OTC desk.

Pros

- 900+ assets, earn products, futures, margin, and bots in one app.

- Low 0.10% spot fees and early listings of newer tokens.

- The widest feature set available to Korean users who want more than spot.

Cons

- Not FIU-registered, so no protection under Korean law and no local recourse.

- No KRW rail, and the app is blocked in Korean app stores.

- Has faced regulatory inquiries and a security incident elsewhere.

2. Upbit

Upbit, run by Dunamu and partnered with K Bank, is the leading domestic exchange and the won anchor most Koreans build around. With 65% to 72% of domestic volume, its KRW books are the deepest in the country, fills are tight, and spot fees sit at 0.25%.

Funding was the simplest of the group. We linked a K Bank real-name account, sent won, and the balance cleared in seconds, though the first withdrawal sat under the mandatory 24-hour hold. Upbit lists about 290 assets, supports staking, and holds most funds in cold storage.

The catch is concentration. Its dominance makes Upbit a single point of failure, and it has drawn regulatory heat, including a September 2025 deposit suspension tied to its bank and an ongoing FIU review.

Pros

- Deepest KRW liquidity in Korea, with the tightest spreads on size.

- Low 0.25% spot fees, clean app, staking, and ISO 27001 with 99% cold storage.

- Smoothest real-name K Bank funding of any platform tested.

Cons

- Market dominance creates concentration and single-venue risk.

- Faced an FIU review and a 2025 deposit suspension tied to its bank.

- Spot only, with no derivatives, margin, or leverage.

.webp)

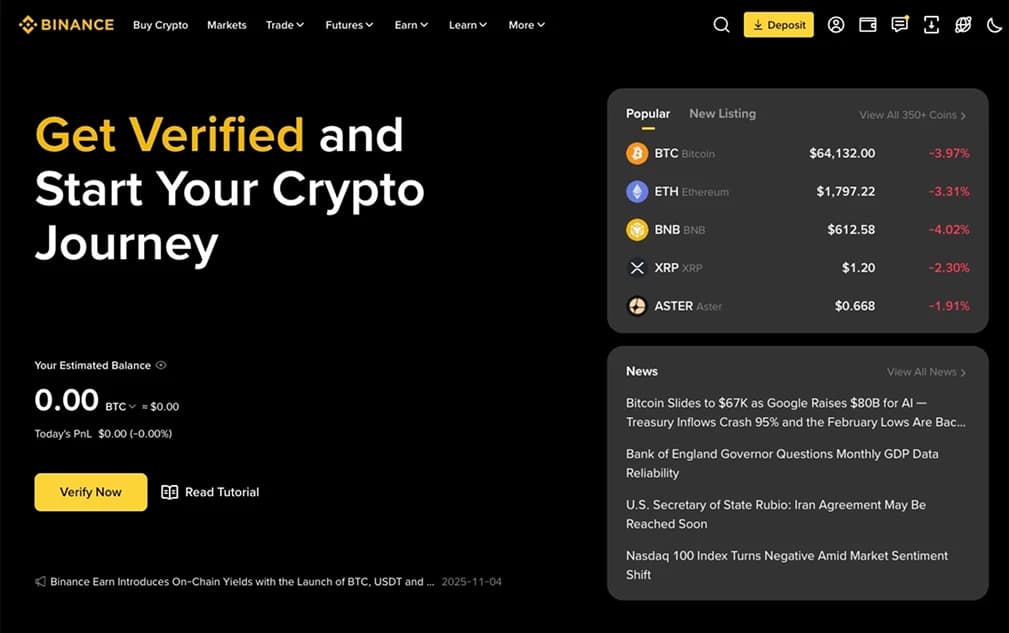

3. Binance

Binance is the other global venue Koreans lean on for what domestic exchanges cannot offer. Deep global liquidity, 0.10% spot fees, and a full derivatives suite make it the default for futures and leverage, and it reportedly earned an estimated KRW 2.73 trillion from Korean users in 2025.

The constraints mirror KuCoin's. No won on-ramp, so funding runs through USDT by P2P or card, and the app was removed from Korean stores during the 2025 and early 2026 sweep. Access is web-based, with its own risks. This applies to all global cryptocurrency exchanges.

Binance is not FIU-registered, so trades sit outside Korean investor protection. The practical setup pairs a licensed domestic exchange for won spot and holdings with Binance, only for the derivatives and global names the local market lacks.

Pros

- Deepest global liquidity and a full derivatives suite at 0.10% spot fees.

- Access to 350+ assets and leverage that no licensed Korean venue offers.

- Strong global security infrastructure and proof of reserves.

Cons

- Not FIU-registered, so no protection under Korean law and no local recourse.

- No KRW rail, and the app is blocked in Korean app stores.

- Using offshore venues carries regulatory and self-custody risk.

4. Bithumb

Bithumb is the cost pick among licensed venues. Its 0.04% fee is the lowest published rate of any FIU-registered Korean exchange, and it has run fee-free campaigns to take share from Upbit. It now holds roughly a quarter of the market and lists 440+ cryptocurrencies.

Bithumb shifted its real-name banking from NH Nonghyup to KB Kookmin Bank on 24 March 2025, forcing existing users to re-link accounts. We funded through KB Kookmin without trouble, and the standard 24 to 72 hour withdrawal hold applied to our first transfer out.

A domestic IPO, reportedly targeting 2028, has sharpened its disclosure and compliance. The offset is a security history that includes past hacks, so the record is worth knowing before committing size.

Pros

- Lowest domestic spot fee at 0.04%, with periodic fee-free promotions.

- Wider listing count than Upbit at around 440 assets.

- IPO preparation has tightened disclosure and compliance.

Cons

- Past security incidents sit on its record.

- The March 2025 bank switch forced existing users to re-link accounts.

- Spot only, with no derivatives available.

.webp)

5. Coinone

Coinone suits investors who prefer a curated asset list over breadth. Founded in 2014 by a security-minded team, it partners with Kakao Bank, keeps most funds in cold wallets with 2FA enforced, and was the first domestic exchange to launch BTC staking.

Funding runs through a Kakao Bank real-name account, convenient given how many Koreans already bank there. Main-market fees are a flat 0.20%, above Upbit and Bithumb, with tiered maker and taker rates for active traders. Large-cap books filled fine in testing.

Its single-digit share alongside Korbit means thinner depth on mid-cap pairs and a quieter listing pipeline. For a buy-and-hold investor wanting fewer speculative names and a clean record, that restraint works in its favor.

Pros

- Curated listings and a strong security-first reputation since 2014.

- Convenient Kakao Bank real-name funding and BTC staking.

- Majority cold storage with 2FA enforced across all accounts.

Cons

- Flat 0.20% main-market fee is higher than Upbit or Bithumb.

- A smaller share means thinner depth on mid-cap pairs.

- Spot only, with a narrower asset range by design.

.webp)

6. Korbit

Korbit was founded in 2013 as Korea's first crypto exchange, partnered with Shinhan Bank, and has never been the victim of a major hack. It leans conservative, with a tight listing policy, ETH staking, an NFT marketplace, and a trading API.

Fees tier by 30-day volume, with maker rates from 0.08% toward zero for heavy traders and taker rates near 0.20% falling with size. We funded through a Shinhan real-name account and found it reliable if less slick than Upbit, with the usual withdrawal hold.

Its weakness is scale. Volumes and liquidity trail the larger venues; the listing count is the smallest here, and the interface feels dated. For a long-term holder, that hardly matters, but active traders will feel the thin books.

Pros

- Korea's oldest exchange with no history of a major hack.

- Volume-tiered fees that reward higher-activity traders.

- ETH staking, an NFT marketplace, and a trading API.

Cons

- Lower liquidity and the smallest listing count among the licensed venues.

- The interface feels dated next to Upbit and Bithumb.

- Spot only, with no derivatives or margin.

.webp)

How to Choose a Crypto Exchange in South Korea

Korea's market is segmented enough that chasing the lowest fee misses the point. Weigh four things before funding anything:

- Know the license line. Only five exchanges with a real-name bank deal, Upbit, Bithumb, Coinone, Korbit, and Gopax, can legally take won and fall under the Virtual Asset User Protection Act. KuCoin and Binance sit outside that perimeter, a risk to price in rather than an automatic dealbreaker.

- Match the bank to the exchange. On a domestic venue, your deposit account must be in your own name at the exact partner bank: K Bank for Upbit, KB Kookmin for Bithumb, Kakao Bank for Coinone, Shinhan for Korbit. Transfers from any other account are auto-rejected.

- Decide if you need derivatives. Spot only points to a licensed domestic venue. Futures, leverage, or the widest altcoin lists point to KuCoin or Binance, with the access and regulatory trade-offs attached.

- Plan around the withdrawal hold. Since May 2025, exchanges must hold crypto withdrawals for 24 to 72 hours after a won deposit to curb voice-phishing fraud. Fund ahead rather than expecting to deposit and move coins the same day.

Crypto and Bitcoin Regulation in South Korea

Korea built its framework around banking control and anti-money-laundering, and tightened it sharply across 2024 and 2025. The pieces that matter:

- VASP registration and real-name accounts: Under the Act on Reporting and Using Specified Financial Transaction Information, every exchange must register with the FIU, hold an ISMS certification, and run real-name verified bank accounts. The single-bank rule is why only five exchanges survived, from roughly 60 before the 2021 deadline.

- Virtual Asset User Protection Act: In force since July 2024, it mandates segregated client funds, cold-storage minimums, and insurance or reserves equal to at least 5% of hot-wallet holdings, with a floor of approximately KRW 3 billion for major exchanges.

- The Travel Rule: Transfers above 1 million won require originator and beneficiary details to pass between VASPs, per FATF guidance. Regulators are weighing whether to extend it below that threshold.

- The crackdown on foreign exchanges: Throughout 2025 and into 2026, the FIU removed unregistered apps such as KuCoin, MEXC, Bybit, OKX, and Binance from Google Play and the App Store.

The takeaway: a licensed Korean venue is legal and protected, while offshore platforms sit outside the regime and are accessed via the web, not the local app stores. Many active Koreans still use them for depth and product range, accepting the trade-off knowingly.

How Does The NTS Tax Crypto?

Individual crypto gains in Korea are currently untaxed, but that is set to change, and the timing has been a political saga.

- The 22% rate from 2027. Gains will be taxed from 1 January 2027 as "other income" at a combined 22%, 20% national plus a 2% local surcharge.

- A low threshold. Only annual gains above 2.5 million won, roughly USD 1,800, are taxable, and the tax hits profit, not transaction value.

- First filings in 2028. Income earned in 2027 is reported in May 2028, with the National Tax Service building reporting systems alongside the five major exchanges.

- A live repeal effort. After three delays, the People Power Party introduced a March 2026 bill to scrap the tax outright, arguing crypto should not be treated more harshly than stocks, and a public petition against it has reached parliamentary review.

Nothing is owed today, but a low-threshold regime is penciled in for 2027 unless lawmakers act first. None of this is tax advice; for anything material, consult a Korean tax professional.

Cryptocurrency Adoption in South Korea

Korea's adoption runs deep and is culturally distinct, and the policy direction turned in 2025. The drivers are specific to the country:

- Scale against population. More than 16 million Koreans, over 30% of the population, use crypto exchanges, and Upbit alone processed around KRW 833 trillion in the first half of 2025, regularly ranking among the world's busiest venues.

- The Kimchi premium. Walled off from global liquidity by capital controls and the real-name system, Korean prices have long traded above overseas exchanges, a gap locals call the "Kimchi premium."

- A pro-crypto administration. Since 2025, President Lee Jae-myung has pushed to legalize spot Bitcoin ETFs, build a won-backed stablecoin to stem capital outflows, phase in corporate accounts, and study pension-fund exposure.

- Institutional onboarding. Corporate trading is rolling out in stages, and the central bank has paused CBDC work in favor of bank-led won stablecoin pilots, signaling deeper integration with traditional finance.

A young, mobile-first population and a structure that channels almost all won activity through a few regulated venues are the load-bearing supports here.

How to Buy Bitcoin in South Korea

Buying Bitcoin in Korea is quick once your real-name account is linked, but stricter than in most countries, because the bank pairing and the withdrawal hold are both fixed.

The steps below cover a licensed domestic exchange, the legal way to turn won into crypto. They assume a resident with a Korean ID, phone number, and bank account; foreigners need an Alien Registration Card and an account at the partner bank.

If derivatives or global altcoins are the goal, run a parallel account on KuCoin or Binance, funded by buying USDT through P2P, and accept that it sits outside Korean investor protection.

- Pick an exchange: Register and complete KYC with your Korean ID and phone number, usually minutes for residents.

- Deposit KRW: Send a won transfer, which lands in seconds, then buy BTC against KRW with a limit order near the spread rather than one-tap instant buy.

- Account for the withdrawal hold: Expect 24 to 72 hours before you can move freshly bought crypto off the exchange after a won deposit. Plan self-custody transfers around it.

- Decide on custody: Active traders can leave coins on the exchange; long-term holders should move to a hardware or mobile wallet. Our best crypto wallets guide covers the options, and always double-check the network and address first.

Final Thoughts

Korea has no single best exchange, only the right fit for the job. For range, earn products, and derivatives, KuCoin offers the most in one app, with Binance close behind in liquidity and futures. Both carry the same caveats: no won rail, no cover under Korean law, and apps in the local stores.

For anything in won, Upbit is the anchor: deepest KRW liquidity, 0.05% fees, and the cleanest real-name funding via K Bank. Keep Bithumb for its 0.04% fee and wider listings, and Coinone or Korbit for curated assets or a spotless security record.

Two facts to keep pinned this year: on a domestic venue, your bank decides your exchange, and a fresh won deposit means a 24 to 72 hour wait before your coins move. Whatever you pick, run a small amount through the full loop before trusting it with size.

Our Methodology

To build this list, we opened accounts the way a Korean trader would: KYC, a real-name partner bank accounts on domestic venues, won funding where possible, P2P on global venues, live spot trades, a withdrawal hold, then funds back out. Five factors set the ranking:

- Trust Score: Our 0 to 5 rating on security and custody record, operating history, reserves and disclosure, and registration status.

- Regulatory Status: FIU registration, ISMS certification, and a real-name bank deal, which place a venue under the Virtual Asset User Protection Act. Upbit, Bithumb, Coinone, and Korbit qualify; KuCoin and Binance do not.

- KRW Funding: Real-name bank funding on domestic venues, tested for settlement speed and the 24 to 72 hour withdrawal hold, plus P2P access on the global ones.

- Full-Loop Cost: Bought and sold the same amount to capture fees and spreads together, not just the headline rate.

- Assets, Liquidity, and Tools: Market and limit orders on major pairs, checked for depth and fills, weighed against staking, yield, derivatives, and other features per user type.

Testing ran from March to June 2026.

Frequently asked questions

.webp)

.webp)