6 Best Crypto Exchanges in USA

If you’re a US resident choosing a crypto exchange in 2026, here’s the fast answer: we’d start with Kraken for most people, Binance.US if fees are your primary concern, and if you’re security-first and happy to pay high costs for tighter controls, Coinbase is the conservative pick.

The goal isn’t to crown a brand; it’s to help you avoid the traps we've seen over and over, like paying a hidden spread on the default buy screen, getting stuck in an ACH hold, or finding out your state blocks a feature you assumed you’d have.

In the sections below, we’ll rank the best US exchanges by who they’re for, then break down fees, funding rails, withdrawal friction, and state availability so you can pick once and move on.

Top Picks: Best Platforms for 2026

- Kraken - Best Overall Crypto Exchange

- Coinbase - Regulated in All U.S. States

- Binance.US - Offers the Lowest Fees

- Uphold - Good Option for Beginners

- Gemini - Invest in Crypto & Stocks

- Crypto.com - Popular Crypto Card

Top Crypto Exchange in the USA - Kraken

Kraken is the best and most trusted crypto exchange in the United States due to its nationwide regulatory compliance, advanced security measures and transparent reserve holdings.

Licenses

Registered with FinCEN (Reg No. 31000270997766)

Available Assets

600+ Cryptocurrencies

USD Deposit Methods

ACH, Cards, Bank Transfers, PayPal & More

Compare Top American Crypto Exchanges

1. Kraken

Kraken, based in San Francisco, is the exchange I’d use when I want one app that can handle simple buys, serious trading, and advanced features. It lists 600+ crypto assets for trading and staking. The platform is licensed by FinCEN and available in every state except New York and Maine.

The US funding flow is straightforward in practice. On desktop or mobile we hit Deposit, select USD, then choose ACH through Plaid, link the bank, and fund without a processing fee. There are additional US Dollar payment methods, including PayPal, Debit card, FedWire, and SWIFT.

Where Kraken earns the best overall label is what you can do after you’re funded. If you’re an active trader, Kraken Pro supports margin trading up to 10x on selected assets. And for long-term holders, Auto Earn pays rewards weekly on eligible assets in supported regions.

Pros

- Kraken Pro feels built for real trading, not one-tap spreads, with 10x leverage available and low spot trading fees starting at 0.25% for makers and 0.40% for takers.

- An OTC desk is available for large orders and private execution.

- Kraken is registered as a Money Services Business with FinCEN (MSB Registration No. 31000239561651).

Cons

- The pro interface can feel like a lot if you only buy once a month.

- Feature access can change by state and product type, so you still need to verify availability. xStocks are not available in the United States.

- ACH deposits can carry a 7-day withdrawal hold, and card/digital-wallet buys can also trigger holds.

2. Coinbase

Coinbase is the one we use when a US reader wants an exchange that’s legal where they live and won’t surprise them later. The exchange says it operates in every US state, holds money transmitter licenses, and has a New York BitLicense, with oversight by NYDFS for its NY approvals.

The tradeoff is cost control. The default buy flow is built for speed, but the better-value path is Advanced Trade where you can place market, limit, and stop-limit orders, run charts powered by TradingView, and actually control execution instead of paying a fat spread.

Product-wise, Coinbase has diverse offerings, including spot trading, recurring buys, the USDC Token, and staking where your location allows it. The key is remembering that eligibility can change by jurisdiction, so I always check the staking rules before assuming it’s available.

Pros

- Coinbase has broad US regulatory coverage and clear compliance disclosures.

- Fully licensed and regulated in all 50 U.S. states; FinCEN registered; holds multiple state money transmitter licenses.

- Coinbase One is the exchange’s subscription service, with zero trading fees up to $10,000/month plus benefits like priority support; USDC rewards in the US are tied to Coinbase One membership.

Cons

- The fees when not using Coinbase Advanced or Coinbase One are extremely high, starting at 2% for spot trading.

- Support can feel slow when you’re stuck in a verification or hold situation.

- Features vary by state and account status, so “available” isn’t always “available for you.”

.webp)

3. Binance.US

Binance.US is the top option if your main goal is to pay as little as possible per trade. The fee schedule is the headline: 0% maker fees on Tier 0 pairs, and it advertises 0.01% taker fees. That’s why it lands in the lowest fees slot, provided you actually use the spot trading screen.

The right way to use Binance.US is to skip any simplified buy flow and head straight to Advanced Trading so you control execution. That’s where you make the low-fee structure count, especially if you’re placing maker orders and letting fills come to you.

Product-wise, it’s more than just spot. Binance.US promotes 190+ assets, 240+ trading pairs, advanced order types, and high-speed APIs. If you’re a yield chaser, it pushes staking hard (ETH, SOL, BNB and 20+ PoS assets), and it positions staking as a major product line on the platform.

Pros

- Very aggressive fee positioning, including 0% maker on select tiers/pairs.

- Binance.US is registered as a Money Services Business with FinCEN under BAM Trading Services Inc. (NMLS ID # 1906829).

- It is highly secure with customer funds held securely on a 1:1 basis within U.S.-based storage facilities.

Cons

- Binance.US has previously paused or limited USD banking rails, so we always treat banking access as something to double-check before committing.

- If you stick to simplified buy flows, you can give back the fee advantage.

- Binance.US is not supported in Alaska, American Samoa, Connecticut, Georgia, Guam, Maine, Northern Mariana Islands, New York, North Carolina, North Dakota, Ohio, Oregon, Texas, U.S. Virgin Islands, Vermont and Washington.

.webp)

4. Uphold

Uphold is the platform we point beginners to when they want to buy crypto without learning an order book on day one. The UX is exactly what newcomers need: one-step trading between any supported assets, so you can move several funds in a single action without juggling multiple screens.

What makes Uphold different is the discovery angle. They’re connected to multiple underlying trading venues and pitch themselves as a way to access a broader range of tokens and sometimes see new listings earlier than more conservative US platforms.

Security and transparency are where Uphold tries to earn trust. They claim they don’t lend out customer assets and publish their assets and liabilities every 30 seconds on the transparency page, which is a rare level of real-time reporting for a retail-facing platform.

Pros

- Uphold is regulated in the U.S. by FinCEN and by several state regulators in 46 states.

- In addition to cryptocurrency, both precious metals and fiat currencies are supported in the same account.

- Instant stake/unstake on 20+ assets, with advertised rewards up to 15.15%.

Cons

- Power users may miss advanced order control compared with pro exchanges.

- Easy swap execution can hide pricing nuances if you don’t watch quotes closely.

- Not the best choice if your main goal is tight spreads as the fees start at 1.2%.

.webp)

5. Gemini

Gemini leans hard into full-reserve custody and regulation. It’s a New York trust company, and that’s a different vibe than “we’re regulated somewhere, trust us.” If you’re security-first, that matters. It operates as Gemini Trust Company, LLC (with an NMLS number published on its site).

If you actually trade, the product to use is ActiveTrader. That’s the interface built for order-book trading rather than one-tap quotes. When we compare costs and execution, ActiveTrader is where Gemini makes sense: you get a trader layout and fee schedule that’s meant for real traders.

Gemini also runs a proper institutional stack, custody, exchange access, and eOTC, which matters if you’re a business, a fund, or even just a high-net-worth buyer. The crypto + stocks angle can apply when Gemini offers equity-style exposure through its broader product ecosystem.

Pros

- Gemini is licensed as a New York trust company and is available in all 50 U.S. states, Washington D.C., and Puerto Rico.

- ActiveTrader brings proper order-book trading and tiered fees.

- Tokenized stocks are offered through a partner on supported accounts.

Cons

- Gemini has had past product fallout (Earn) that’s worth remembering when you judge risk tolerance.

- Product availability can vary by jurisdiction and account type.

- For many users, it’s secure and steady, but doesn’t offer the widest selection of assets or features.

6. Crypto.com

Crypto.com is the most suitable option if the card is the reason you’re signing up. The Visa Credit Card is the hook because you earn crypto back on everyday spend, and the best reward tiers come with Level Up requirements (a subscription or CRO staking for 12 months on some tiers).

Crypto.com markets zero-fee USD deposits using ACH and wire, and it also supports buying crypto using Apple Pay/Google Pay. In the app, we test it the same way every time: open Fiat Wallet → Deposit → USD → ACH/Wire, then do a small test deposit before moving serious money.

Where Crypto.com gets bigger than “card + buy button” is product breadth. The app lists 400+ assets, has Crypto Earn for yield-style rewards on supported assets, and includes Onchain tools for self-custody. For advanced users, it also promotes US CFTC-regulated derivatives inside the app.

Pros

- Strong card-first product design with Visa Signature benefits.

- Clear US availability guidance (49 states; check state access first).

- Good fit if you want one app for buying crypto and spending rewards.

Cons

- Not available everywhere in the US (New York is the big one).

- Best rewards tiers can come with lockups or program requirements.

- If your priority is tight execution and advanced orders, a pro exchange may suit you better.

How to Choose a Crypto Exchange in the USA (2026)

In the US, the best exchange is the one that lets you link a bank account cleanly, fund with ACH at low cost, buy at tight pricing (not hidden spreads), and withdraw to your bank or wallet without getting stuck in review.

When we test US platforms, we start where Americans actually get burned: state availability, banking rails, and fees that hide in the default buy screen.

Step 1: Confirm your state is supported

Before making a deposit, we try signing up and checking two things:

- State support: some features and even full access can change by state. If the app lets you create an account but blocks funding or withdrawals later, that’s a waste of time.

- KYC flow quality: go to Profile/Account → Verification and watch for red flags: repeated ID requests, pending loops, or address checks that fail even when your documents match.

Step 2: Check relevant licensing

We don’t take regulated marketing at face value. We look for clear disclosures that the exchange is:

- Registered as a money services business with FinCEN (this is the baseline for US-facing platforms handling transfers).

- Licensed as a money transmitter at the state level (issued by state financial regulators; the exchange should list its state license coverage or provide a license lookup path).

- If you’re in New York, authorized by New York State Department of Financial Services (BitLicense or a NY trust charter). New York is a fast filter because it’s strict.

Rule we follow: if we can’t easily find the exchange’s US compliance footprint in plain language, we don’t use it as our primary account.

Step 3: Verify funding rails that work in the US

For most Americans, the practical on-ramp is ACH. Users should always check that their preferred deposit method is supported.

- ACH (preferred): lower cost, good for recurring buys, but expect new-account holds before withdrawals.

- Wire: faster finality, fewer ACH hold surprises, but more manual and sometimes bank-fee heavy.

- Debit card: instant but usually the worst value (higher fees) and the most likely to get declined.

If a platform pushes you into Instant Buy as the default and makes advanced trading hard to find, assume you’ll pay more over time.

Step 4: Confirm security measures

US platforms talk a big game. We verify the settings that protect you when something goes wrong:

- Authenticator app or security key support (we avoid SMS-only setups).

- Withdrawal controls: address whitelisting (if offered), withdrawal confirmations, device management.

- Transparency signals: incident history, operational status page, and proof-of-reserves or clear custody disclosures.

If we can’t find these in under five minutes, we don’t keep meaningful balances there.

Step 5: Understand the fees

The biggest cost for US users is often not the published trading fee, it’s the spread on simple buy/sell screens.

What we do to avoid these high fees:

- Switch to the Advanced/Pro trading view or use spot trading.

- Use limit orders on pairs like BTC/USD or BTC/USDC.

- Treat “free trading” claims with caution if pricing is worse than the order book.

Also factor in:

- ACH withdrawal timing/holds.

- Network fees when withdrawing crypto (don’t move tiny amounts on expensive chains).

If you want a fast shortcut, pick the exchange that has reliable ACH + an accessible advanced trading screen, then use limit orders so you control the price instead of accepting whatever the app quotes.

Crypto & Bitcoin Regulation in the USA

In the US, crypto regulation isn’t one rulebook and one regulatory body; it’s a set of overlapping systems that decide what you can trade, how exchanges move dollars, what gets reported to the government, and where a platform can legally operate.

When we test US exchanges, this is what regulation usually means in practice: KYC checks, AML monitoring, Travel Rule messaging, limits on certain products, and state-by-state availability that can change the recommendation overnight.

The main regulators investors need to be aware of are:

- The Securities and Exchange Commission (SEC) focuses on securities laws, disclosures, and whether a token/product falls under securities rules (often shaping what gets listed and what products get pulled back).

- The Commodity Futures Trading Commission (CFTC) oversees derivatives markets and has asserted authority in crypto-related derivatives enforcement; lawmakers keep pushing proposals that would expand its role for spot markets.

- The Financial Crimes Enforcement Network (FinCEN) sets and enforces AML expectations under the Bank Secrecy Act for many crypto businesses, which shows up as onboarding checks and compliance holds.

If you just want the turning points, this timeline highlights the handful of US regulatory moments that changed exchange access, token listings, and what products Americans can use.

- 2013: FinCEN issues guidance that becomes the baseline for AML/KYC expectations for many crypto businesses in the US.

- 2014: Internal Revenue Service says crypto is treated as property for federal tax purposes, setting the foundation for taxable trades and reporting.

- 2015: New York State Department of Financial Services launches the BitLicense regime, making New York the toughest state for exchange access and product scope.

- 2017: SEC publishes the DAO Report, a landmark moment that pushes many token offerings into securities-law risk analysis.

- 2022: The White House issues Executive Order 14067, kicking off a whole-of-government push on digital asset policy and coordination.

- 2024: The SEC approves the first spot bitcoin exchange-traded products for US listings, pulling bitcoin exposure deeper into traditional brokerage wrappers.

- 2025: The White House revokes Executive Order 14067, signaling a policy shift at the top even as the agency patchwork remains.

- 2025: The GENIUS Act becomes law and creates a federal framework for payment stablecoins, including supervision requirements and explicit AML obligations for issuers.

- 2026: Reuters reports Senate momentum around a market-structure bill that would hand the U.S. Commodity Futures Trading Commission a larger role in overseeing spot crypto markets, with stablecoin-related fights still slowing progress.

It’s important to mention that even if a platform is available in the U.S., state rules can still change your experience. The biggest example is New York, where “virtual currency business activity” generally requires a BitLicense or approval from the New York State Department of Financial Services (NYDFS).

What this means: if you’re in NY, your shortlist often shrinks fast, and product availability can look different than it does in most other states. It’s important to check if your selected exchange is licensed to operate in your state.

How Does The IRS Tax Cryptocurrency?

For tax purposes, crypto is handled by the Internal Revenue Service (IRS) under the U.S. Department of the Treasury. The IRS is the one that sets reporting expectations and audits returns.

In our testing and review work, crypto activity usually falls into two categories:

- Capital Gains Tax: Applies when you dispose of crypto (sell, trade, spend). The IRS treats most crypto as property, so gains/losses work like stocks.

- Ordinary Income Tax: Applies when you receive crypto as income (paid in crypto, staking rewards, mining, many airdrops). That income can later create capital gains/losses when you sell.

- Net Investment Income Tax (NIIT) of 3.8% for higher-income filers on certain investment income.

Crypto Tax Rates in the USA

Capital Gains:

- Short-term (held 1 year or less): taxed at ordinary income rates.

- Long-term (held more than 1 year): generally 0% / 15% / 20%, depending on your taxable income.

Ordinary Income:

The federal brackets use 7 rates, varying from 10% - 37%.

- 10%: $0 – $12,400

- 12%: $12,401 – $50,400

- 22%: $50,401 – $105,700

- 24%: $105,701 – $201,775

- 32%: $201,776 – $256,225

- 35%: $256,226 – $640,600

- 37%: $640,601+

If you want your reporting to hold up, we recommend exporting all exchange CSVs (trades, deposits, withdrawals, rewards) and keeping the raw files. This is a practical overview, not personal tax advice. All American investors should consult their tax advisor for the most up-to-date guidance regarding cryptocurrency.

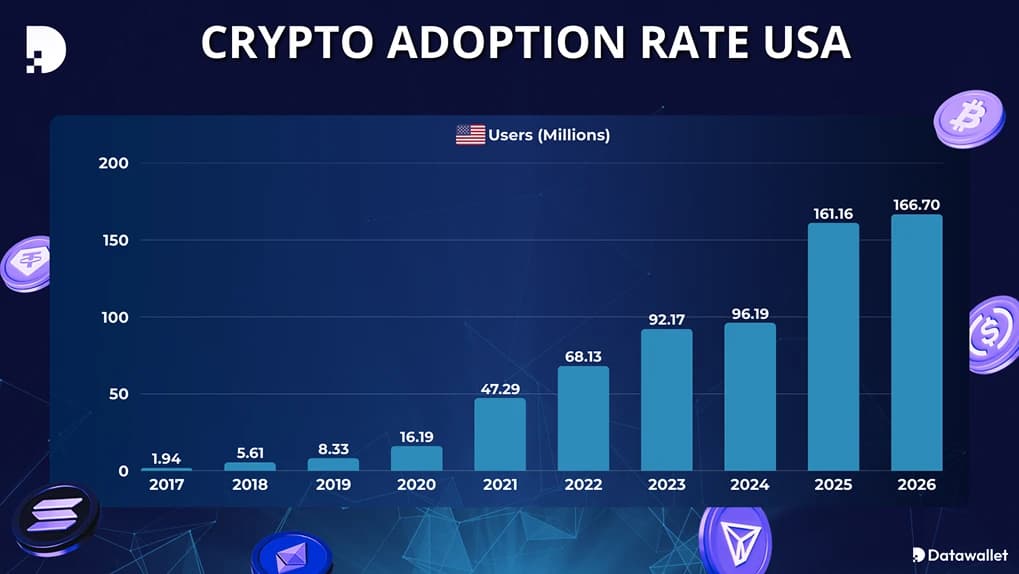

Cryptocurrency Adoption in the United States

Most US users we see are not treating crypto like a checkout method. They’re buying Bitcoin/Ethereum and a handful of majors, then either holding or trading. Ownership is stronger among younger adults and men (older survey patterns remain consistent).

Chainalysis reports that North America accounts for 26% of all transaction activity in the period they studied and around $2.3 trillion in received transaction value (July 2024–June 2025), with the US ranking near the top globally.

Here's a snapshot of cryptocurrency adoption in the USA according to Statista:

- Crypto Holders: 166.7 million Americans in 2026.

- Population Percentage Holding/Using Crypto: 48.5% user penetration by the end of 2026.

- Crypto Market Revenue in the US: about $17.5 billion.

How to Buy Bitcoin in the U.S

Buying Bitcoin in the US in 2026 is simple if you use the correct method. The biggest friction isn’t hitting “Buy”, it’s getting an ACH deposit to clear without a hold, avoiding the high-spread Instant Buy screen, and making sure you can withdraw to your bank without triggering a review.

- Choose a regulated exchange: During signup, we confirm our state is supported and the exchange is licensed with FinCEN and relevant state regulators.

- Complete identity verification (KYC): Go to Profile/Account → Verification and finish the prompts. Expect ID upload (driver’s license or passport), a selfie/liveness check, and sometimes an address match.

- Fund your account: We use ACH for lower fees, then plan for an ACH hold on new accounts. Debit cards are faster but often cost more and can get declined.

- Buy Bitcoin: We switch to the Advanced/Pro or Spot Trading interface and buy BTC/USD (or BTC/USDC) using a limit order to avoid paying a wider spread.

A hardware wallet (Ledger or Trezor) is our default for long-term storage. A reputable software wallet works fine for smaller amounts, but the point is the same: you control the keys, not the exchange.

Final Thoughts

If you’re picking a US crypto exchange in 2026, treat this like a checklist, not a brand contest: start with Kraken for a balanced setup, choose Binance.US only if you’ll actually use the order book to earn the fee advantage, and lean Coinbase when your top priority is broad state coverage and a conservative compliance posture.

Before you deposit real money, do three quick tests, confirm your state isn’t blocked, run a small ACH deposit and withdrawal to see if holds hit your account, and place one limit order on the advanced screen so you don’t get clipped by the “instant buy” spread.

Then lock it down with app-based 2FA, keep long-term coins in a wallet you control, and save your CSV exports from day one so taxes don’t become a guessing game later.

Frequently asked questions

.webp)