Best Decentralized Perpetual Exchanges in 2026

Summary: Decentralized perpetual exchanges (perp DEXs) have moved from experimental venues to serious infrastructure, with monthly volumes now exceeding $1 trillion and capturing roughly a quarter of the global futures market.

The 2026 story is no longer crypto-on-crypto leverage. Thanks to Hyperliquid's HIP-3 upgrade, traders are moving size into tokenized oil, silver, gold, and the S&P 500, fully on-chain, 24/7.

This analysis ranks the leading perp DEXs in 2026 by liquidity, open interest, execution quality, fees, and product breadth:

- Hyperliquid: The Dominant Perp DEX and the Home of On-Chain TradFi

- Lighter: Zero-Knowledge Perp DEX with Provable Execution

- EdgeX: Institutional-Grade Execution on StarkEx

- Aster: Binance-Backed High-Leverage Multi-Chain DEX

- Jupiter Perps: The Leading Solana-Native Perp Exchange

- dYdX: The Longest-Running On-Chain Derivatives Venue

- ApeX: Multi-Asset zkL2 with Tokenized Stocks

Best Decentralized Perps Platform - Hyperliquid

Hyperliquid ranks as the top decentralized perps DEX, combining unmatched liquidity, 40x leverage, and the first 24/7 on-chain markets for oil, silver, and the S&P 500.

Daily Volume

Over $10 billion in 24h volume

Fees

Maker 0.015%, Taker 0.045%

Supported Tokens

180+ perpetual pairs including BTC, ETH, SOL, plus HIP-3 TradFi assets

Best Perp DEXs in 2026

The table below summarises where traders are deploying capital right now, what each platform charges, and the features that set them apart.

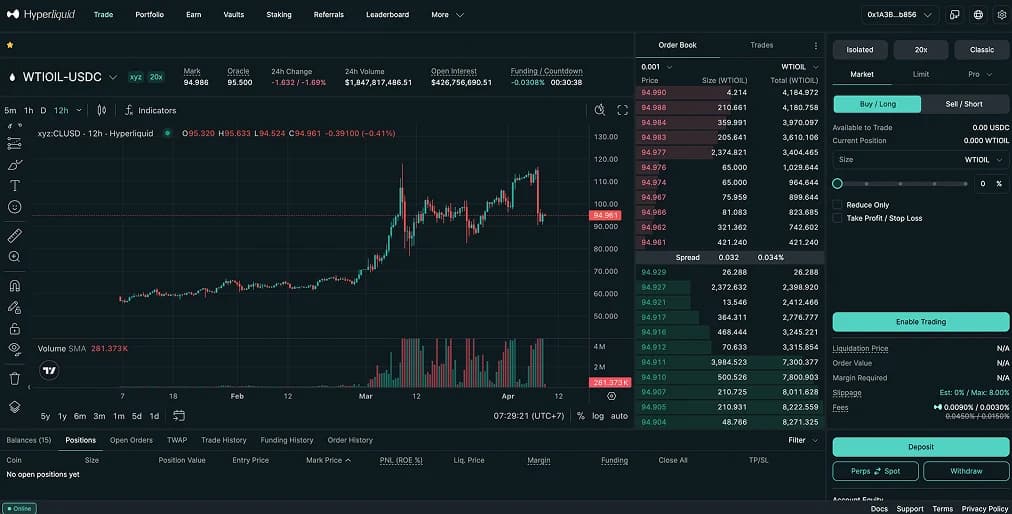

1. Hyperliquid: The Dominant Perp DEX

Hyperliquid is the clear market leader in decentralized perpetual trading. Its purpose-built Layer 1, powered by HyperBFT consensus, delivers one-block finality and quotes tighter BTC perp spreads than Binance. Its share of global perp DEX volume climbed from 36% in January 2026 to roughly 44% by late March, and it holds close to two-thirds of all sector open interest.

The 2026 edge is HIP-3, the Builder-Deployed Perpetuals framework launched October 2025. Trade[XYZ] was the first deployer, listing 24/7 markets for crude oil, Brent, gold, silver, and tokenized US equities. On March 18, 2026, S&P Dow Jones Indices officially licensed the S&P 500 to Trade[XYZ], making Hyperliquid the only venue offering an officially licensed S&P 500 perpetual.

HIP-3 open interest hit a record $2.3 billion on April 6, 2026, with crude oil alone clearing $1.99 billion in daily volume during February's Iran conflict. Six of Hyperliquid's top 10 markets are now RWA pairs, and 97% of protocol fees flow into the Assistance Fund for automated HYPE buybacks.

Pros

- Deepest liquidity and tightest spreads of any perp DEX, rivalling top-tier CEXs on BTC and ETH.

- HIP-3 unlocks 24/7 trading on oil, silver, gold, and the officially licensed S&P 500.

- Close to $1 billion in annualised revenue flowing into aggressive HYPE buybacks.

- Proven track record through the October 2025 liquidation cascade without vault losses.

Cons

- HIP-3 markets rely on deployer-managed oracles and are not backstopped by the native HLP vault.

- Maximum leverage capped at 40x on crypto, lower than several competitors.

- Currently inaccessible to US-based traders through the main front-end.

2. Lighter: Zero-Knowledge Perp DEX with Provable Execution

Lighter is a zk-rollup perp exchange that publishes validity proofs for every trade, order, and liquidation. It raised $68M at a $1.5B valuation in November 2025 from Founders Fund, Ribbit, Haun Ventures, and Robinhood Ventures, then completed its December 30 TGE distributing 25% of LIT supply. LIT peaked at $3.70 before settling near $1.00 by April 2026.

By March 2026, Lighter ranked fourth with roughly $65B monthly volume and $679M open interest, well behind Hyperliquid's $178B. Retail still pays zero fees while Premium accounts pay 0.002% maker and 0.02% taker, and a February LIT Fee Credits system lets traders access premium tiers without large stakes.

The 2026 roadmap is aggressive. Lighter shipped Partner Attribution in March, letting third parties build custom frontends on its matching engine, launched a Commodities Challenge for WTI, gold, and silver perps, and is prepping a mobile app and Lighter EVM rollout.

Pros

- Zero fees for retail, ultra-low Premium tiers for institutional flow.

- Every trade and liquidation cryptographically verified via zk proofs.

- Backed by Founders Fund, Ribbit, Haun, and Robinhood at a $1.5B valuation.

- Expanding into commodity perps and third-party frontends via Partner Attribution.

Cons

- Monthly volume fell roughly 70% post-TGE as incentive flows dried up.

- LIT down over 70% from its December 2025 all-time high.

- Limited asset depth beyond majors, with RWA markets still early.

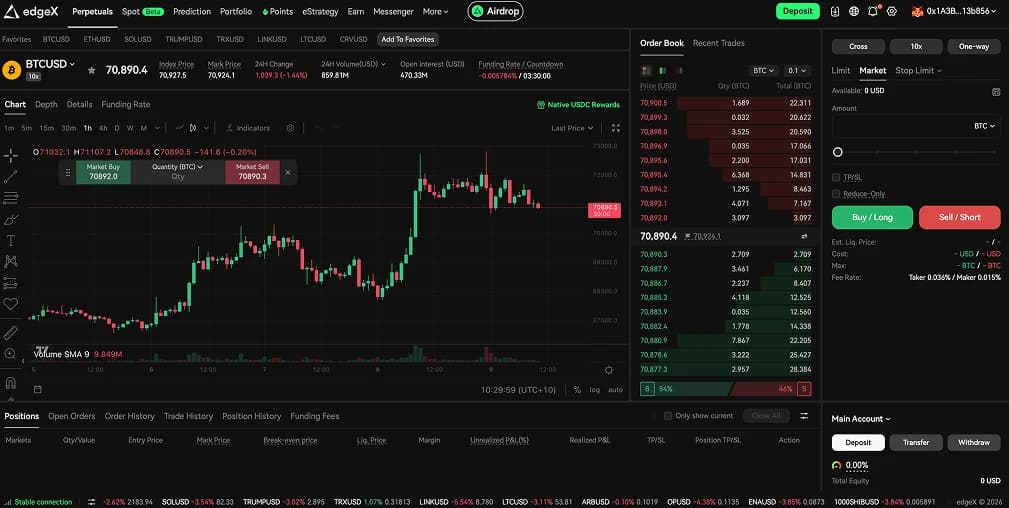

3. EdgeX: Institutional-Grade Execution on StarkEx

EdgeX was incubated by Amber Group and launched in November 2024 on StarkWare's StarkEx engine. By late March 2026 it had cleared over $861B in cumulative volume across 300,000+ users, ranking second by daily volume with roughly $3B in trading and $10M in BTC depth within 1bp. It briefly surpassed Hyperliquid in daily fees, hitting $1.3M in a single Q1 session.

The EDGE token TGE landed March 31, 2026 at a $700M pre-market FDV, with 25% airdropped. Circle Ventures made a strategic investment in February, with native USDC deployment planned for the upcoming EDGE Chain, an Arbitrum Orbit L2 replacing the StarkEx validium.

V2 stretches EdgeX beyond crypto perps. Spot trading went live in December 2025, US stock perpetuals launched in January, and Polymarket prediction markets integrated natively in February. EdgeX now runs 176+ pairs across crypto, equities, and prediction markets, with an eStrategy vault offering yield via the eLP pool.

Pros

- Sub-10ms latency and 200,000+ orders per second, briefly leading Hyperliquid on daily fees.

- Expanded into spot, US stock perpetuals, and native Polymarket prediction markets.

- Circle Ventures backing with native USDC coming to EDGE Chain.

- $10M BTC depth within 1bp, rivalling top centralized venues.

Cons

- Migration from StarkEx to Arbitrum-based EDGE Chain carries execution risk.

- OI-to-volume ratio of 0.23 signals shorter trades than Hyperliquid's 0.64.

- EDGE token post-TGE price action remains unproven.

4. Aster: Binance-Backed High-Leverage Multi-Chain DEX

Aster launched its own privacy-focused Layer 1 on March 17, 2026, moving from BNB Chain to a purpose-built mainnet with zero gas, sub-50ms blocks, and a 100,000+ TPS target. The chain uses ZK encryption and stealth addresses by default, making position hunting and wallet tracing structurally impossible. Aster holds #2 by 7-day volume at $20.39B with nearly $2B in open interest.

ASTER trades between $0.65 and $0.80 at a $1.88B market cap after a December 2025 burn of 77.8M tokens worth $80M. The team has bought back 165.8M tokens for over $173M, though ASTER has failed to break $0.80 resistance as Hyperliquid widens the market share gap.

Feature depth is strong. Shield Mode enables private high-leverage trading, TWAP orders reduce slippage, and Degen Mode strips opening fees. Tokenized equity perps cover Apple, Tesla, Nvidia, and Meta at 50x, forex runs at 200x, and crypto majors reach 1001x. Staking, governance, and a Smart Money copy-trading tool all land in Q2 2026.

Pros

- Privacy Layer 1 with encrypted orders and stealth addresses by default.

- #2 perp DEX by 7-day volume with $20B+ weekly activity.

- Deflationary tokenomics with $173M+ in cumulative ASTER buybacks.

- Multi-asset coverage across crypto, forex, and tokenized US equities.

Cons

- DefiLlama previously delisted Aster's data over volume transparency concerns.

- ASTER has repeatedly failed to break $0.80 despite heavy buyback pressure.

- 1001x leverage creates meaningful liquidation risk for retail.

5. Jupiter Perps: The Leading Solana-Native Perp Exchange

Jupiter Perps is the derivatives product inside Jupiter, Solana's dominant aggregator with roughly 95% of Solana aggregator volume and over half of total Solana DEX activity. Perps averaged $277M daily in March 2026, down from $425M February peaks, with the broader platform holding $2.6 to $3B in TVL. Leverage reaches 100x on SOL, ETH, and wBTC, with select pairs up to 250x.

The product routes through the Jupiter Liquidity Provider Pool (JLP) and charges hourly borrow fees rather than funding rates. Traders pay 0% maker and 0.06% taker, and any SPL token deposits as collateral through auto-routing. The Dove Oracle, co-designed with Chaos Labs, delivers zero price impact regardless of trade size.

2026 has been product-heavy. Jupiter launched JupUSD in January through an Ethena Labs partnership, backed by BlackRock's BUIDL fund, with $750M of JLP collateral scheduled to convert in Q2. Polymarket integrated in February, Swap API V2 shipped in March, and the delayed Jupuary 2026 airdrop distributes 400M JUP in May.

Pros

- Zero maker fees and no funding rate, replaced by transparent hourly borrow costs.

- Any SPL token accepted as collateral via aggregator auto-routing.

- Deep integration with the Jupiter DeFi stack including JupUSD, Lend, and Polymarket.

- Dove Oracle delivers zero price impact regardless of trade size.

Cons

- Only three tradable assets (SOL, ETH, wBTC), far fewer than Hyperliquid or dYdX.

- Daily volume dropped from $425M in February to $277M in March 2026.

- No TradFi or RWA markets to compete with Hyperliquid's HIP-3 offering.

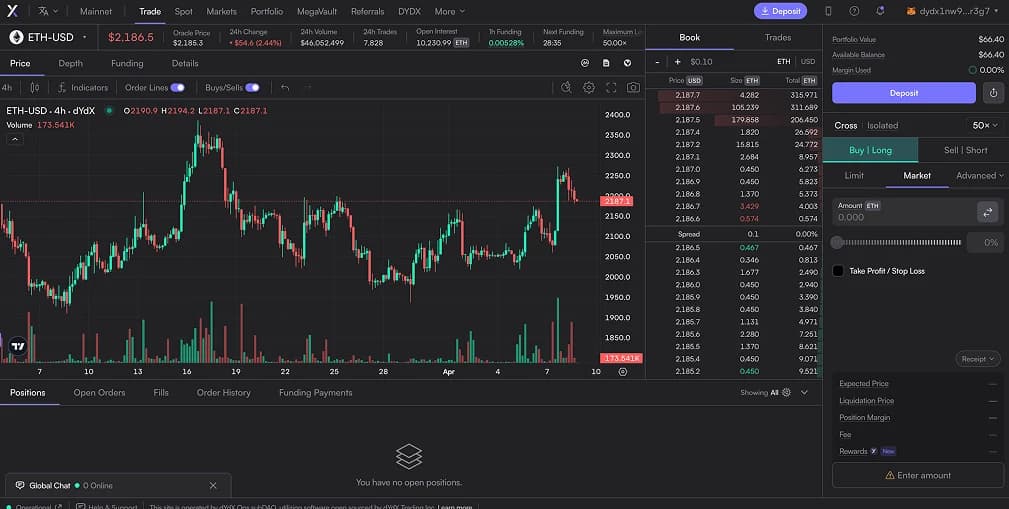

6. dYdX: The Oldest On-Chain Derivatives Venue

Founded in 2017 by former Coinbase engineer Antonio Juliano, dYdX holds a clean security record after $1.5 trillion in lifetime volume. In December 2025 it launched its first spot market with SOL, opening the platform to US-based traders for the first time. Monthly volume sits at $25 to $30B with $300 to $400M in TVL.

The community approved a tokenomics upgrade allocating 75% of net protocol revenue to DYDX buybacks, up from earlier experimental levels. Combined with the 2026 pivot to RWA perpetuals starting with Tesla synthetic equity, this creates a direct link between trading activity and token demand. Protocol v8.2 recently shipped with matching engine and risk upgrades.

Traders get 200+ perpetual markets, up to 25x leverage on BTC and ETH, advanced order types, and full API support. Fee tiers offer maker rebates up to -0.011% and taker fees from 0.05%, and dYdX ran a zero-fee promotion throughout December 2025 to onboard US users.

Pros

- Nine-year clean security record, the longest of any perp DEX.

- First spot market (SOL) opened the platform to US traders in December 2025.

- 75% of net protocol revenue now flows into DYDX buybacks.

- Planned RWA perpetuals starting with Tesla synthetic equity in 2026.

Cons

- Monthly volume has fallen well behind Hyperliquid, Lighter, and Aster.

- Cosmos app-chain adds deposit friction for EVM-native traders.

- DYDX has underperformed as volume migrated to faster competitors.

7. ApeX: Multi-Asset zkL2 with Tokenized Stocks

ApeX Protocol runs on a zkLink-based Layer 2 at 10,000 TPS with gas-free trading across six chains including Ethereum, Arbitrum, Base, and Solana. Cumulative volume has passed $200B since launch, with 150+ markets spanning crypto, tokenized US stocks (NVDA, TSLA, META), and leveraged prediction contracts, all backed by first-in-class portfolio margin and multi-collateral support.

In November 2025, ApeX upgraded to Chainlink Data Streams across five chains to unlock low-latency RWA perpetuals, and Prediction Markets launched in July 2025 with up to 20x leverage. Base fees start at 0.02% maker and 0.05% taker, dropping to 0% maker / 0.025% taker at VIP tiers. A Privy integration now allows email-based account creation.

The APEX Token Buyback Program has repurchased roughly $9.6M through late November 2025 using Omni trading fees. Ahead, ApeX is building its own Omni AppChain as a dedicated settlement layer for cross-chain intent routing, alongside continued expansion of prediction markets and vault yield products.

Pros

- 150+ perpetual markets across crypto, tokenized stocks, and prediction markets.

- First DEX to offer portfolio margin with multi-collateral support.

- Chainlink Data Streams powers low-latency RWA perps across 5 chains.

- Email account creation via Privy removes most Web3 onboarding friction.

Cons

- Daily volume and open interest remain a fraction of Hyperliquid's.

- APEX buyback program is modest versus Hyperliquid or Aster.

- Omni AppChain and RWA expansion still execution risks rather than live differentiators.

The 2026 Perp DEX Themes You Need to Know

HIP-3 and the Move to 24/7 TradFi Markets

The biggest shift in on-chain derivatives this year has been real TradFi assets arriving on perp DEXs, almost entirely through Hyperliquid's HIP-3 framework. Qualified builders can now deploy markets for commodities, equities, forex, and indices permissionlessly, provided they post the HYPE bond and manage their own oracles.

The implications are significant. When oil prices moved 30% over the weekend of the Iran strikes in February 2026, CME and ICE were closed and Hyperliquid was the only venue in the world pricing crude in real time. When the S&P 500 reacts to Sunday-night macro news, the Trade[XYZ] contract trades through the gap rather than waiting for Monday open. A BTC, HYPE, and ETH portfolio can now short oil, hedge equity exposure, or go long gold from a single account.

The End of the Points Farming Meta

2025 was defined by incentive-driven volume. Aster briefly reported $100 billion in daily volume, Lighter processed $232 billion in the 30 days before its TGE, and airdrop farmers generated trillions in wash trades. After Lighter's December 2025 token launch, volumes across the sector fell sharply as points chasers unwound positions. Hyperliquid, which never leaned heavily on points, saw its market share climb from 20% to over 44% through this unwind.

Open interest tells the real story. Hyperliquid's OI-to-volume ratio sits near 0.64, meaning most of its volume reflects capital held overnight. Lighter and Aster historically ran ratios below 0.18, characteristic of flipping rather than durable positions. Capital is consolidating at venues that generate real revenue over subsidised activity.

Deflationary Tokenomics and ETF Speculation

Hyperliquid's buyback mechanic, in which 97% of protocol fees flow to the Assistance Fund for open-market HYPE purchases, is one of the most aggressive value accrual structures in crypto. Arthur Hayes has laid out a bull case targeting $150 for HYPE, citing real revenue, disciplined supply, and genuine trading activity.

The Grayscale spot HYPE ETF filing, alongside similar filings from Bitwise and 21Shares, signals institutional interest in perp DEX economics without direct protocol exposure. Approval timelines remain unclear, and US-based traders still cannot access Hyperliquid's front-end directly.

CLOB Dominance Over AMM Perps

The earlier generation of perp DEXs such as GMX and Gains Network used AMM or peer-to-pool designs where pooled liquidity faced traders directly. These models were easy to bootstrap but struggled with capital efficiency, oracle risk, and adverse selection during volatile moves. Every 2026 leader runs a central limit order book instead, which is why they deliver tight spreads, sub-second finality, and execution quality that previously required centralized infrastructure.

Perp DEX vs Perp CEX: Which Is Better for Traders?

Centralized exchanges still dominate global perpetual volume. Binance alone processed over $2 trillion in Q1 2025, and the top five CEXs together account for the vast majority of all perpetual futures activity. For deep liquidity on long-tail altcoin pairs and regulated fiat on-ramps, CEXs remain hard to match.

The decentralized side has closed the gap faster than most analysts predicted. Perp DEX market share grew from 3.5% to over 26% in the past year, driven by Hyperliquid's execution quality, HIP-3 TradFi markets, and the failure of several smaller centralized venues. For maximum liquidity on majors and fiat deposits, the best centralized futures exchanges still win. For self-custody, 24/7 TradFi access, and exposure to the fastest-growing infrastructure in crypto, perp DEXs are increasingly where serious capital goes.

Trading Fees on Perp DEXs

Fees on decentralized perpetuals come in five forms, and managing them is essential to staying profitable.

- Trading Fees. Maker orders that add liquidity are almost always cheaper than taker orders. Hyperliquid charges 0.015% maker and 0.045% taker at base tier; Lighter offers zero fees to retail entirely. Using limit orders instead of market orders is the single biggest fee optimisation most traders overlook.

- Funding Rates. Funding rates align perpetual prices with spot through periodic payments between longs and shorts. Hyperliquid updates funding hourly with a cap of ±0.05% per interval.

- Liquidation Fees. Triggered when margin falls below maintenance. Hyperliquid uses a fixed 50% maintenance margin model, stricter than many competitors but better at protecting the insurance fund during volatile moves.

- Network Fees. Vary by chain. Hyperliquid charges no network fees on its own L1. Arbitrum-based venues cost $0.10 to $0.20 per transaction. Solana-based Jupiter costs fractions of a cent.

- Slippage. Determined by order book depth. Hyperliquid and EdgeX offer the tightest spreads; smaller venues can see meaningful slippage on large orders.

Risks of Using Decentralized Perpetual Exchanges

Perp DEXs solve custody risk but introduce their own hazards that traders should understand before deploying capital.

- Smart Contract Vulnerabilities. Even audited protocols can be exploited. The GMX $42M incident showed how logic flaws in pooled liquidity models can drain markets within minutes.

- Governance and Admin Key Compromise. The April 2026 Drift Protocol hack drained $285 million in 12 minutes through a DPRK-linked social engineering campaign that compromised developer devices and obtained multisig approvals via pre-signed "durable nonce" transactions. Governance hygiene, timelocks, and signer security matter as much as smart contract audits.

- Oracle Manipulation. Venues relying on Pyth, Chainlink, or Redstone depend entirely on oracle accuracy. HIP-3 markets are particularly sensitive because deployers manage their own price feeds.

- MEV and Front-Running. EigenPhi tracks over 10,000 manipulated trades per day across DeFi, translating into billions in annual extraction. Venues with proper sequencer design or zk-based matching are more resistant.

- Regulatory Uncertainty. The SEC and CFTC treat most perpetuals as unregistered derivatives, the FCA bans crypto derivatives for UK retail, and MiCA may soon regulate front-ends serving EU users.

- Recovery Limitations. Self-custody means no chargebacks, no support hotlines, and limited recourse if a private key is compromised. A quality hardware wallet reduces this risk considerably.

Final Thoughts

Decentralized perpetual exchanges crossed a meaningful threshold in 2026. With HIP-3, they have become the only places in the world where anyone can trade oil, silver, gold, and the S&P 500 on a 24/7 basis with verifiable on-chain settlement. That capability is genuinely new in global markets, and the volume growth confirms traders are taking advantage of it.

Hyperliquid's lead is substantial and backed by real revenue, real open interest, and infrastructure that centralized exchanges now benchmark themselves against. Lighter, EdgeX, and Aster each occupy defensible niches. The weaker models built around points farming and wash-trading have already started to fade.

For traders entering this market, favor venues with deep liquidity and sustainable economics, size positions conservatively, and remember that self-custody means the security of your funds is ultimately your responsibility.

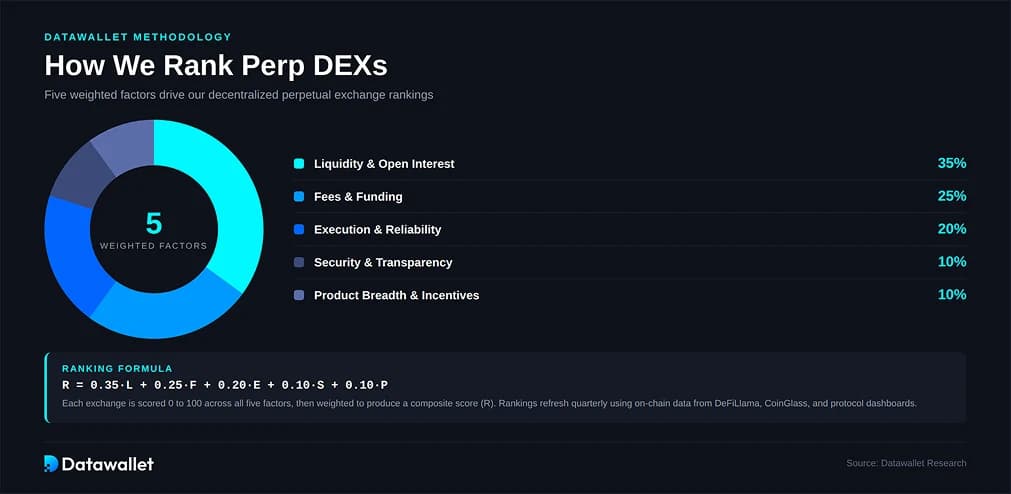

Our Methodology for Perp DEX Rankings

Our rankings are built from objective on-chain data and public protocol dashboards, with the goal of identifying which perp DEXs traders can actually rely on for deep liquidity, fair execution, and sustainable economics. The evaluation window covers the most recent 90 days across BTC, ETH, and SOL perpetual markets, plus HIP-3 and RWA markets where applicable.

- Liquidity and Open Interest (35%) - 24-hour volume, committed open interest, and order book depth, sourced from DeFiLlama, CoinGlass, and protocol dashboards. Open interest is weighted heavily because it reflects capital at risk rather than wash-trading for points.

- Fees and Funding (25%) - Maker and taker costs, funding rate stability, and effective cost at retail size.

- Execution and Reliability (20%) - Latency, uptime, and settlement finality, including how venues handled the October 2025 liquidation cascade.

- Security and Transparency (10%) - Audit history, exploit record, and quality of public on-chain metrics.

- Product Breadth and Incentives (10%) - Range of markets offered, asset classes beyond crypto, and sustainability of rewards programs.

Frequently asked questions

.webp)