Tokenization Statistics & Trends for 2026

Summary: Tokenisation moves traditional assets like Treasuries, credit, gold and shares onto blockchain rails, where they settle in seconds and stay usable inside DeFi.

Around $31.4 billion of real-world assets now sit on-chain excluding stablecoins, up four to five times in a year, and Boston Consulting Group projects the market could reach $16 trillion by 2030.

Six asset classes have each passed a billion dollars, private credit and tokenised Treasuries lead, and regulated launches from BlackRock, Franklin Templeton and JPMorgan have pulled the sector from pilot stage into production.

Top 10 Tokenization Statistics for 2026

These benchmarks frame the tokenisation market midway through 2026.

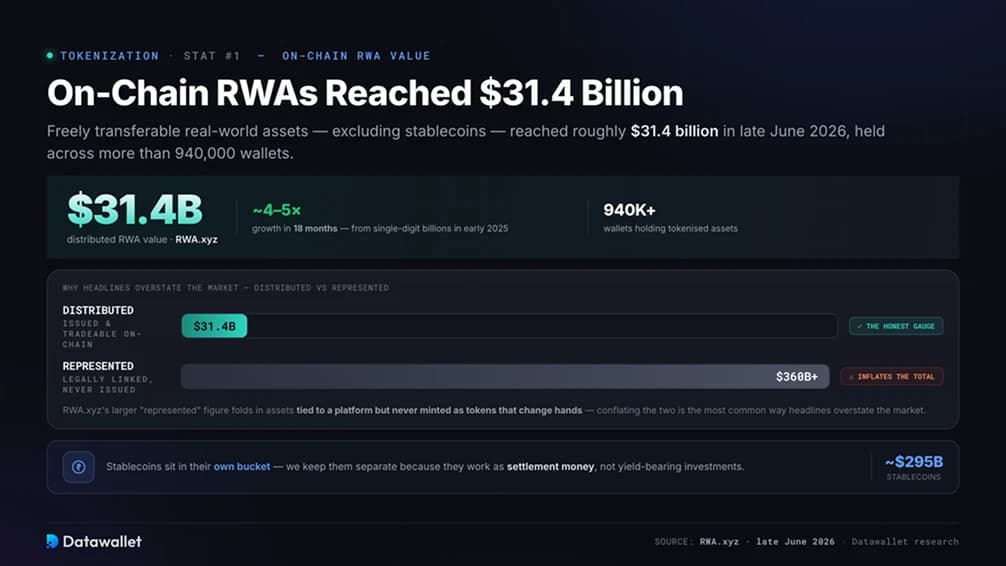

1. On-Chain Real-World Assets Reached $31.4 Billion

Tokenised real-world assets, counted as freely transferable tokens excluding stablecoins, reached roughly $31.4 billion in late June 2026 on RWA.xyz, held across more than 940,000 wallets. The base sat in single-digit billions at the start of 2025, so the sector has grown four to five times in eighteen months.

That figure needs a caveat. RWA.xyz also reports a far larger represented value above $360 billion, which folds in assets legally linked to a platform but never issued as tokens that change hands on-chain. The honest gauge of what investors can buy and sell is the distributed figure near $31.4 billion, and conflating the two is the most common way headlines overstate the market.

Stablecoins sit in their own bucket worth close to $295 billion. We keep them separate because they work as settlement money rather than yield-bearing investments, a split covered in our stablecoin statistics breakdown.

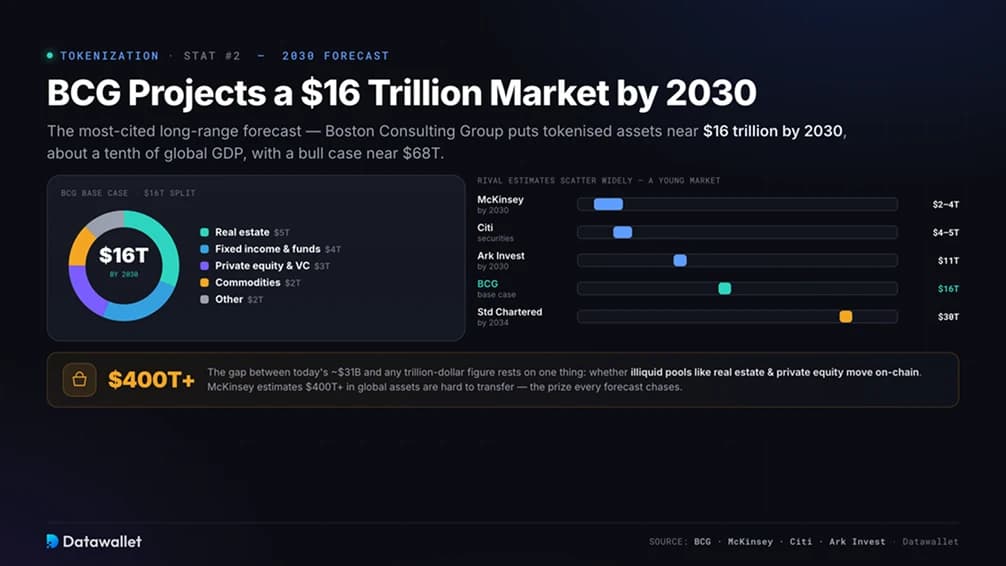

2. BCG Projects a $16 Trillion Tokenization Market by 2030

The most cited long-range forecast belongs to Boston Consulting Group. In work published with private-markets exchange ADDX, it put tokenised assets near $16 trillion by 2030, around a tenth of global GDP. That total splits into roughly $5 trillion of real estate, $4 trillion of fixed income and funds, $3 trillion of private equity and venture capital, $2 trillion of commodities and $2 trillion of other assets, with a bull case near $68 trillion.

Rival estimates scatter widely, a sign of how young the market is. McKinsey lands at $2 trillion to $4 trillion by the decade's end, Citi sees $4 trillion to $5 trillion in tokenised securities, Standard Chartered has floated $30 trillion by 2034, and Ark Invest's Big Ideas 2026 report models $11 trillion by 2030, still under 1.4% of all global financial assets.

The gap between today's ~$31 billion and any trillion-dollar figure rests on one variable, whether large illiquid pools like real estate and private equity actually move on-chain. McKinsey estimates more than $400 trillion in global assets are hard to transfer or price, and that pool is the prize every forecast chases.

3. Six Asset Classes Have Each Passed a Billion Dollars

For most of its early life the sector was effectively one product, tokenised US Treasuries. That has changed. By 2026 at least six categories had independently cleared a billion dollars on-chain, spanning private credit, gold and commodities, US Treasuries, corporate bonds, non-US sovereign debt and institutional alternative funds. Tokenised equities have since joined them.

This breadth matters for durability. A market resting on one asset class can be knocked sideways by a single regulatory decision, while one spread across six is far harder to dislodge. The mix also shows capital favouring familiar instruments first, government and corporate debt, before reaching harder-to-tokenise assets like property and private equity.

4. Tokenised Treasuries Anchor the Market at Around $14 Billion

Short-dated government debt is the entry point for institutions testing on-chain finance, with tokenised Treasury and money-market products worth roughly $14 billion. These tokens pay 3.3% to 3.6%, settle near-instantly, and work as collateral or on-chain cash in place of idle stablecoins.

The leaderboard is institutional. Circle's USYC sits near $3.1 billion, BlackRock's BUIDL holds about $2.2 billion across eight chains after reaching DeFi via Uniswap in February 2026, Ondo's USDY clears $2.1 billion, and Franklin Templeton's BENJI line, behind the first US-registered mutual fund to use a public blockchain as its record, adds $2.4 billion across share classes.

In May 2026, Ondo, JPMorgan, Mastercard and Ripple completed the first cross-border redemption of a tokenised Treasury, settling in under five seconds.

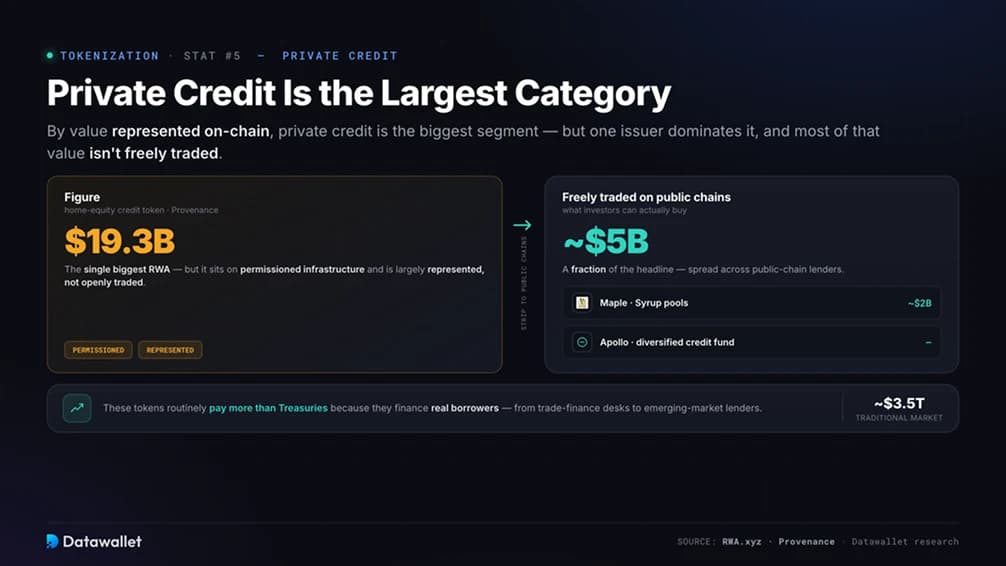

5. Private Credit Is the Largest Category, Led by Figure

By value represented on-chain, private credit is the biggest segment, and one issuer dominates it. Figure's home-equity credit token shows around $19.3 billion on the Provenance blockchain. That value sits on permissioned infrastructure and is largely represented rather than openly traded, so it inflates the category well beyond what investors can freely buy.

Strip back to tokens that move on public chains and the figure is smaller, near $5 billion, spread across lenders like Maple, whose Syrup pools hold roughly $2 billion, and Apollo's diversified credit fund. These tokens routinely pay more than Treasuries because they finance real borrowers, from trade-finance desks to emerging-market lenders, against a traditional market near $3.5 trillion globally.

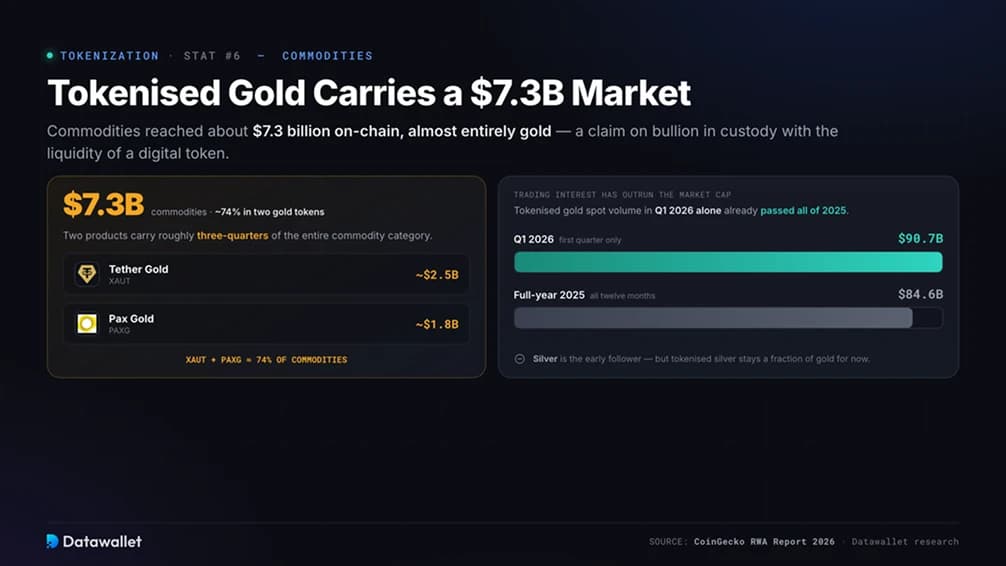

6. Tokenised Gold Carries a $7.3 Billion Commodity Market

Commodities reached about $7.3 billion on-chain, almost entirely gold. Tokenised gold gives holders a claim on bullion in custody with the liquidity of a digital token, and two products carry roughly three-quarters of the segment, Tether Gold near $2.5 billion and Paxos Gold around $1.8 billion.

Trading interest has outrun the headline market cap. Tokenised gold spot volume hit $90.7 billion in the first quarter of 2026, already past the $84.6 billion logged across all of 2025. Silver is the early follower, though tokenised silver products stay a fraction of gold for now.

7. Tokenised Equities Hit $1 Billion Faster Than Any Prior Category

The breakout retail story of 2026 is tokenised stocks. The global market for tokenised equities reached roughly $1.5 billion, crossing its first billion in about eight months. Stablecoins took around three years to hit that mark and tokenised Treasuries about two, which shows how fast demand arrived.

Ondo Global Markets holds the lion's share, more than 70%, with over 260 tokenised US stocks and ETFs across Ethereum, Solana and BNB Chain and more than $18 billion in cumulative volume. Each token is backed one-for-one by shares held at a US-registered broker-dealer and tracks total return including dividends. The limit is important, holders get economic exposure to the share price, not legal ownership or voting rights, which stay with the custodian.

Distribution is widening fast. Ondo's tokens went live in MetaMask in February 2026, Broadridge brought on-chain proxy voting to more than 250 tokenised stocks, and a fresh batch of Ondo-tokenised equities and ETFs landed in June. The most liquid names mirror retail favourites, Tesla, Circle and NVIDIA.

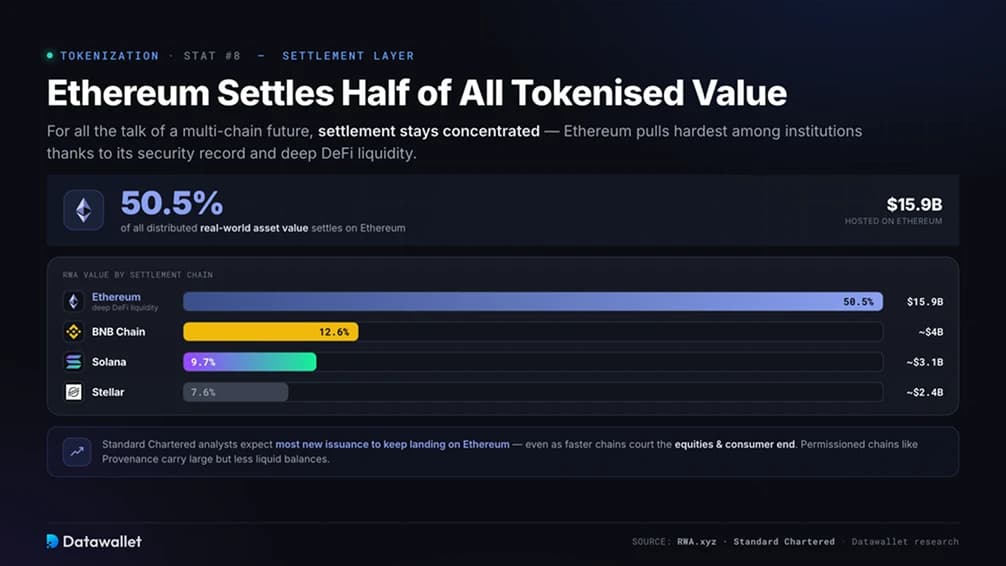

8. Ethereum Settles Half of All Tokenised Asset Value

For all the talk of a multi-chain future, settlement stays concentrated. Ethereum hosts about $15.9 billion of distributed real-world asset value, a 50.5% share, pulling hardest among institutions thanks to its security record and deep DeFi liquidity.

The chasing pack is spread thin. BNB Chain holds around $4 billion (12.6%), Solana about $3.1 billion (9.7%) and Stellar near $2.4 billion (7.6%), while permissioned chains like Provenance carry large but less liquid balances. Standard Chartered analysts expect most new issuance to keep landing on Ethereum, even as faster chains court the equities and consumer end.

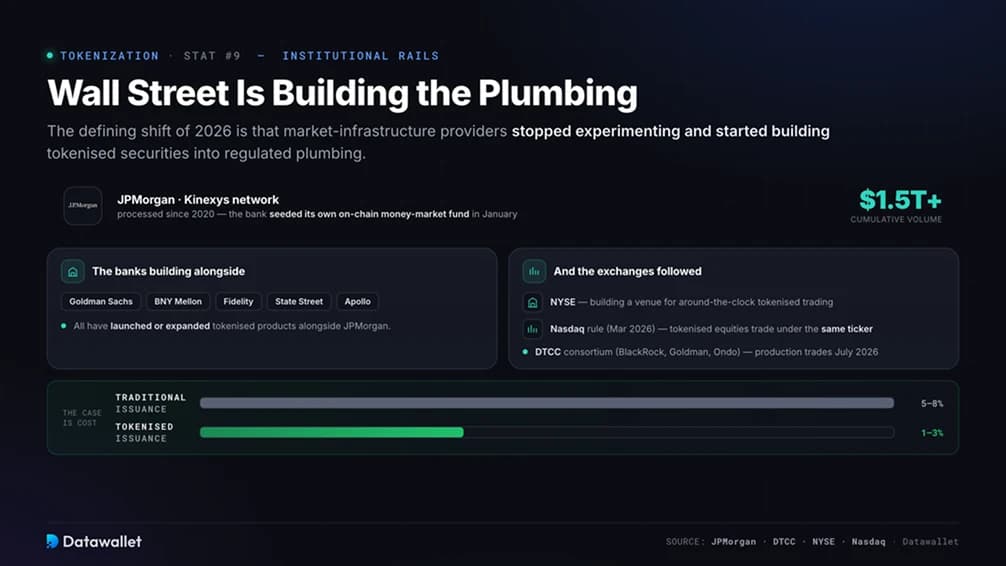

9. Wall Street Is Building the Tokenization Plumbing

The defining shift of 2026 is that market infrastructure providers stopped experimenting and started building. JPMorgan's Kinexys network has processed more than $1.5 trillion in cumulative volume since 2020, and the bank seeded its own on-chain money-market fund in January. Goldman Sachs, BNY Mellon, Fidelity, State Street and Apollo have all launched or expanded products alongside it.

The exchanges followed. The NYSE is building a venue for around-the-clock trading of tokenised securities, the SEC approved a Nasdaq rule change in March 2026 letting tokenised versions of listed equities trade under the same ticker and economic rights, and the DTCC formed a tokenised-securities consortium with BlackRock, Goldman Sachs and Ondo, with production trades due in July 2026.

The case these firms make is cost, traditional issuance fees run an estimated 5% to 8% against 1% to 3% for tokenised issuance.

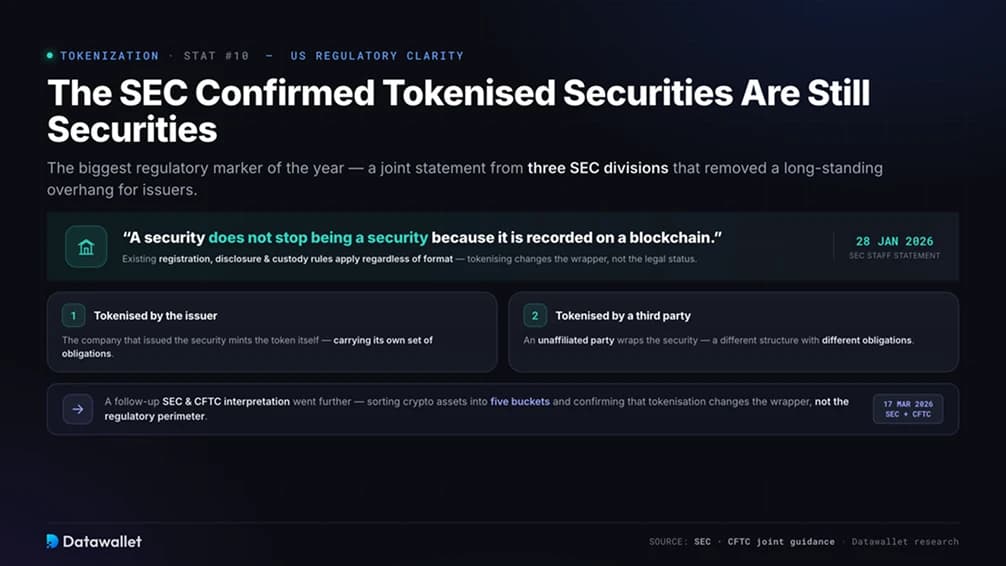

10. The SEC Confirmed Tokenised Securities Are Still Securities

The biggest regulatory marker came on 28 January 2026, when staff from three SEC divisions issued a joint statement on tokenised securities. The core message is blunt, a security does not stop being a security because it is recorded on a blockchain, and existing registration, disclosure and custody rules apply regardless of format.

The statement set out two structures, securities tokenised by the issuer and those tokenised by unaffiliated third parties, each carrying different obligations. It was staff guidance rather than a Commission rule, but it removed a long-standing overhang for issuers. A follow-up SEC and CFTC interpretation on 17 March 2026 went further, sorting crypto assets into five buckets and confirming that tokenisation changes the wrapper, not the regulatory perimeter.

What Is Asset Tokenisation?

Asset tokenisation issues a blockchain token that represents ownership of, or economic exposure to, an off-chain asset. The underlying instrument, a Treasury bill, a gold bar, a share or a loan, is held by a regulated custodian, and a smart contract mints tokens that track its value and, where relevant, its income.

The structure usually runs through a legal wrapper. An issuer places the asset in a special-purpose vehicle, a platform issues tokens against it, and payments like interest or dividends pass back to holders on-chain or through periodic distributions. Compliance rules, such as restricting holders to verified investors, can be coded into the token so they travel with it.

Tokenisation changes how an asset moves while leaving its legal substance untouched. The token can settle in seconds, trade around the clock, split into fractions, and plug into lending or collateral markets, while the asset it represents stays what it was.

Which Assets Are Being Tokenised?

The market has settled into a handful of categories, each with a different yield profile, liquidity level and risk surface.

- Government securities: Tokenised US Treasuries and money-market funds, the largest distributed category, paying yields around 3.3% to 3.6% with deep institutional backing.

- Private credit: Loan pools financing businesses and consumers, the biggest segment by represented value but concentrated on permissioned rails, offering higher yields and thinner liquidity.

- Commodities: Almost entirely gold, with silver emerging, giving on-chain exposure to bullion held in vaults.

- Equities and ETFs: Tokenised stocks tracking listed shares, the fastest-growing retail category, offering price exposure rather than shareholder rights.

- Corporate and non-US debt: Tokenised corporate bonds and sovereign debt outside the US, each now past a billion dollars.

- Alternative and private funds: Tokenised private equity, venture and reinsurance products aimed at qualified investors, including early sovereign-wealth-fund issuance.

- Real estate: The most retail-friendly pitch and the slowest to scale, since tokenising property gives fractional economic exposure more readily than legal title.

Our roundup of the best RWA projects covers the leading platforms building across these categories.

How Is Tokenisation Regulated?

Regulation has been the gating factor for institutional adoption, and 2026 brought the clearest rules yet across major jurisdictions.

- United States: The SEC's January 2026 staff statement confirmed tokenised securities fall under existing securities law, and a March interpretation with the CFTC mapped crypto assets into five categories. The GENIUS Act set the rules for the stablecoins that settle these trades, while the broader CLARITY Act advancing through the Senate would divide oversight between the two agencies.

- European Union: MiCA governs crypto-asset markets, and the European Central Bank began accepting DLT-based assets as eligible collateral for Eurosystem credit operations from 30 March 2026, a meaningful signal of central-bank acceptance.

- United Kingdom: The Financial Conduct Authority is finalising rules for tokenised assets and stablecoin issuance, treating qualifying tokens as money-like instruments rather than speculative products.

- Asia: Singapore, Hong Kong and Japan run dedicated regimes, and Japan's Financial Services Agency is moving to reclassify crypto as financial products, with a proposed tax cut from 55% to 20% that could unlock dormant domestic capital.

Across jurisdictions the message is the same. Tokenisation alters the plumbing of markets without rewriting the law that governs the assets moving through it.

What Could Slow Tokenisation Down?

The growth is real, but several constraints will decide which forecasts land. We see liquidity as the most underrated.

- Thin secondary markets: Most tokenised assets are held rather than traded, and large transfers tend to cluster around institutional batch sizes rather than continuous market activity. Putting an asset on-chain does not create buyers for it.

- Represented versus distributed value: Headline totals lean on represented figures that include assets sitting on permissioned chains, so the tradeable market is smaller than the biggest numbers suggest.

- Legal ownership gaps: Many tokens, including tokenised equities, convey economic exposure without legal title or voting rights, and most jurisdictions still require traditional transfer for genuine ownership changes.

- Custody and oracle dependency: A token only behaves like its underlying asset if the custodian holds the real thing and the price oracle stays accurate. A failure in either link breaks the peg to reality.

- Concentration: Single issuers dominate the largest categories, Figure in private credit and Ondo in equities, which leaves the market exposed to platform-specific risk.

- Smart-contract and regulatory risk: On-chain code can carry undiscovered flaws, and rules still differ sharply across borders, complicating cross-jurisdiction issuance.

Final Thoughts

Tokenisation spent 2024 and 2025 proving it could work and 2026 proving it could scale. A market worth a few billion dollars in early 2025 now carries more than $31 billion in tradeable on-chain value, six asset classes have each passed a billion, and the institutions that once dismissed public blockchains are now building on them.

The direction looks settled even if the destination does not. Whether the market reaches BCG's $16 trillion or McKinsey's $2 trillion by 2030 depends on how fast illiquid assets migrate and how deep secondary markets become, both downstream of the regulatory clarity that arrived this year.

The number that matters is the ratio of trading to holding rather than the headline market cap. The day tokenised assets trade as readily as the shares and bonds they represent is the day tokenisation stops being a sector and becomes how markets settle by default. Until then, the smart read separates distributed value from represented value, and yield-bearing assets from the stablecoins that move them.

Our Methodology

This article draws on live on-chain dashboards, institutional research, regulator publications and issuer data to assess tokenisation in 2026.

- On-chain data: RWA.xyz for distributed and represented asset value, holder counts, network share and individual product sizes, cross-checked against issuer disclosures.

- Market forecasts: Boston Consulting Group with ADDX, McKinsey, Citi, Standard Chartered and Ark Invest for long-range projections, presented as a range rather than a single number.

- Regulatory sources: The SEC's tokenised-securities statement, the SEC and CFTC joint interpretation, and EU and Asian regulator materials for jurisdiction-specific treatment.

- Institutional activity: Public announcements and filings from BlackRock, Franklin Templeton, JPMorgan, the DTCC, Ondo and major exchanges for product launches and infrastructure moves.

- Snapshot caveat: Many figures come from live dashboards, so values shift as issuers mint or redeem tokens and market prices move.

Frequently asked questions

.webp)