Ondo Finance Explained: Tokenization, Treasuries & ONDO Tokenomics

Summary: Ondo Finance is a real-world asset platform that moves U.S. Treasuries, money market funds, and public equities onto blockchains as fully-backed, yield-bearing tokens. Its core products are OUSG and USDY for Treasury exposure, and Ondo Global Markets for tokenized stocks and ETFs.

By mid-2026 Ondo held roughly $3.5 billion in total value locked, controlled more than 70% of the tokenized equity issuer market, and ran a full set of SEC registrations acquired through Oasis Pro. The ONDO token governs the protocol, though its value capture stays unresolved ahead of a planned fee-switch vote.

Ondo Finance Overview

Ondo is the largest issuer of tokenized U.S. Treasuries and tokenized equities, combining institutional-grade asset management with its own SEC-licensed brokerage stack and a purpose-built settlement chain.

Total Value Locked

~$3.5 billion across all products in 2026

Tokenized Equity Share

70%+ of the issuer market

ONDO Supply

10 billion fixed maximum, ~4.87 billion circulating

What is Ondo Finance?

Ondo Finance is a real-world asset (RWA) platform that issues blockchain tokens backed one-for-one by traditional financial instruments. Rather than inventing crypto-native yield, it packages returns from short-term U.S. government debt and, more recently, listed equities into tokens that trade on public chains around the clock.

The platform runs as two halves. An asset-management arm operates the tokenized funds, while a technology arm builds the protocols, bridges, and chain that move those tokens between networks. That split lets Ondo hold regulated securities through licensed entities while still shipping permissionless DeFi infrastructure.

Three product lines define the business in 2026. OUSG and USDY give holders exposure to U.S. Treasury yield, Ondo Global Markets offers tokenized stocks and ETFs, and Ondo Chain provides the institutional settlement layer beneath them. Combined assets sat near $3.5 billion across chains in early 2026, among the largest of any RWA issuer.

Its backers read like a TradFi roster. Venture support came from Founders Fund, Pantera Capital, and Coinbase Ventures, while its Treasury products plug into BlackRock's tokenized money market fund. Ondo was founded in 2021 by Nathan Allman, a former Goldman Sachs structured-products banker, and is overseen by the Ondo Foundation, a nonprofit based in the Cayman Islands.

How Does Ondo Finance Work?

Ondo's model is straightforward: every token it issues is a claim on a real asset held off-chain by a regulated custodian or fund. Tokens are minted when value comes in, redeemed when it leaves, and their on-chain value tracks the underlying. The products differ in what backs them, who can hold them, and how yield reaches the holder.

1. Tokenization and Backing

Each product wraps a pool of regulated assets, then mints tokens representing ownership claims on it. The structure keeps the on-chain token close to the value of what backs it.

The backing model works through these components:

- Custody: Underlying Treasuries, fund shares, and equities are held by regulated custodians and broker-dealers, not by the smart contract, keeping the assets inside existing legal frameworks.

- Minting: Tokens are created when investors deposit stablecoins or fiat, with the protocol allocating the proceeds into the relevant fund or security.

- Redemption: Holders can burn tokens to redeem the underlying value, with several products supporting near-instant 24/7 redemption rather than traditional settlement windows.

- Pricing: On-chain prices track net asset value or accrued interest, keeping tokens tightly aligned with the assets behind them.

- Reserves: Third-party attestations and fund reporting confirm each token series stays fully backed, a requirement for the institutional users Ondo targets.

2. How Yield Reaches Holders

Ondo's Treasury products pay yield in two formats that change how the return shows up in a wallet. Both reflect short-term U.S. interest rates, not DeFi incentives.

The two yield mechanics are:

- Accumulating tokens: Yield compounds into a rising token price, so one token is worth slightly more each day while the balance stays the same. OUSG and standard USDY use this approach.

- Rebasing tokens: Yield arrives as additional tokens distributed to the wallet, keeping the price near a dollar while the balance grows. The rUSDY and rOUSG variants work this way.

- Conversion: Holders can switch between accumulating and rebasing versions through Ondo's token converter without slippage, choosing whichever form suits collateral use or accounting.

3. Eligibility and Access

Securities law, not Ondo, dictates who can hold each token, producing a tiered system where the most regulated product is the most restricted.

Access splits along these lines:

- OUSG: Restricted to U.S. Qualified Purchasers, structured as a 3(c)(7) fund offered under Regulation D Rule 506(c), with a minimum investment historically around $5,000 for instant transactions.

- USDY: Open to retail and institutional investors in eligible non-U.S. regions without accreditation, subject to a lock-up of roughly 40 to 50 days before tokens become transferable.

- Onboarding: Both require identity verification and wallet connection before minting, after which assets can be tracked and moved like any other on-chain token.

Ondo Finance's Core Products

Ondo's catalog has grown from two Treasury wrappers into a full-stack platform spanning cash management, equities, derivatives, and lending. The products below carry most of its assets and activity.

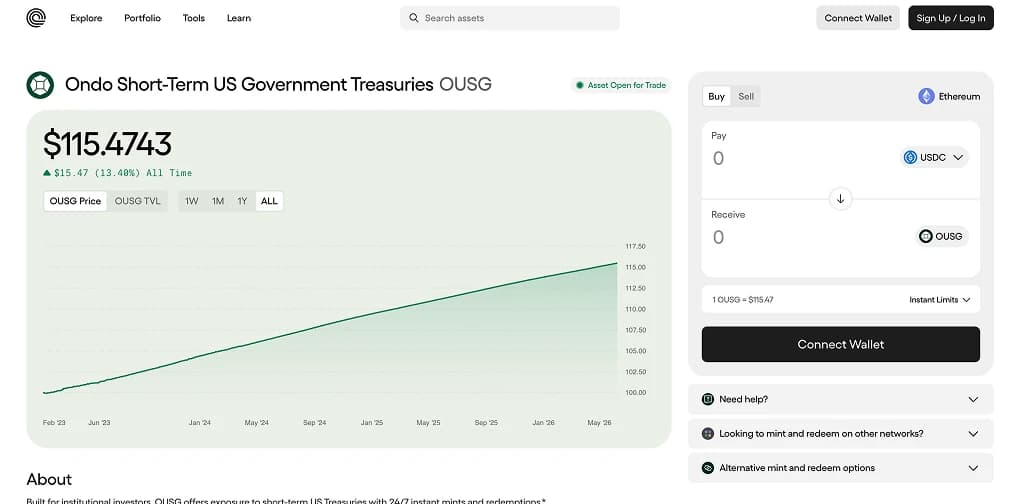

1. OUSG: Tokenized U.S. Treasuries

OUSG (Ondo Short-Term US Government Treasuries) is the institutional cash-management product, giving qualified investors tokenized exposure to short-dated government debt with 24/7 minting and redemption.

- Backing: OUSG allocates primarily to BlackRock's BUIDL tokenized money market fund, alongside Franklin Templeton, Fidelity, WisdomTree, and Wellington vehicles, plus stablecoins and bank deposits for liquidity.

- Yield: Returns float with short-term Treasury rates, in the low-to-mid 3% range in early 2026, after a 0.15% management fee.

- Liquidity: Subscriptions and redemptions clear in USDC and Ripple's RLUSD, and Ondo is the single largest holder of BUIDL.

- Reach: Available across Ethereum, Solana, Polygon, and the XRP Ledger, holding roughly $700 million in assets in 2026.

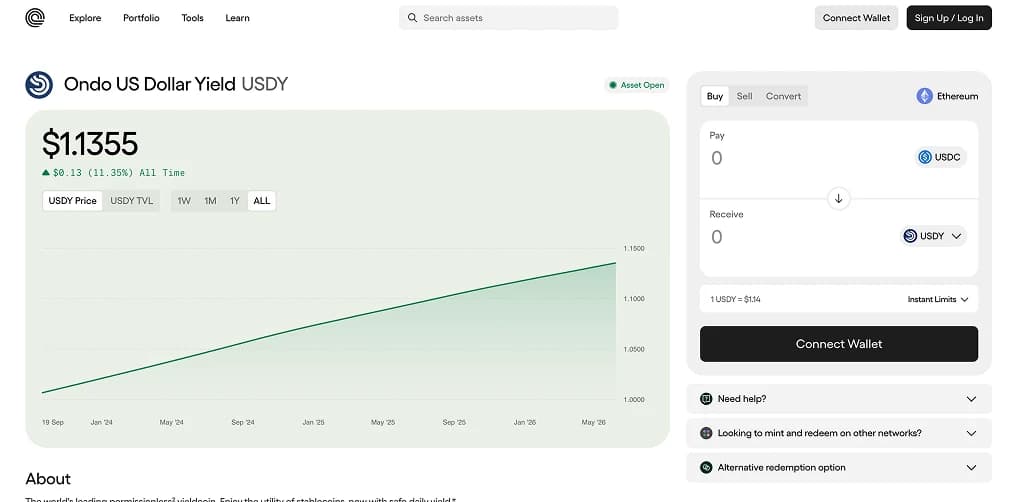

2. USDY: A Yield-Bearing Dollar Token

USDY (US Dollar Yield Token) is the accessible counterpart to OUSG, a tokenized note delivering dollar yield to non-U.S. investors without qualified-purchaser status.

- Structure: USDY is a senior claim on a portfolio of short-term Treasuries and bank deposits held by Ondo USDY LLC, a Delaware bankruptcy-remote entity with equity subordination as a buffer for holders.

- Yield: The variable rate tracks short-term Treasury yields, around 4.5% APY in spring 2026, across its accumulating and rebasing versions.

- Distribution: USDY is the most chain-spread tokenized Treasury product, with supply across Ethereum, Solana, Mantle, Sui, and Aptos, making it a common building block for cross-chain dollar yield.

- Scale: Supply ran near $700 million in 2026 across more than 16,000 holder addresses, with deep secondary liquidity on decentralized venues.

This dual setup is why Ondo features in discussions of the safest yield-bearing stablecoins, though USDY is technically a note, not a pegged stablecoin.

3. Ondo Global Markets: Tokenized Stocks and ETFs

Ondo Global Markets (OGM) is the product that reshaped Ondo in 2026. It offers tokenized stocks and ETFs to non-U.S. users, each token backed by real shares held with a U.S.-registered broker-dealer and settled through the Depository Trust Company.

- Catalog: OGM lists more than 260 tokenized U.S. stocks and ETFs, spanning blue-chip names, growth equities, and broad-market index funds, all tracking total return including dividends.

- Scale: The platform crossed $1 billion in TVL in roughly eight months after launch, a first for any tokenized stocks venue, then pushed past $1.17 billion with cumulative trading volume nearing $20 billion.

- Distribution: Tokens reach users through Binance, Bitget, MetaMask, and Blockchain.com across Solana, Ethereum, and BNB Chain, with KYC and AML applied at the access layer.

- Recognition: Binance admitted OGM securities for trading on its regulated multilateral trading facility in Abu Dhabi Global Markets, and a Broadridge partnership added proxy-voting support for tokenized shareholders.

4. Ondo Perps and Supporting Infrastructure

Ondo extended into derivatives with Ondo Perps, launching June 9, 2026, which lets non-U.S. traders take leveraged positions on tokenized equities. It rounds out a suite that also includes lending and bridging.

- Ondo Perps: Offers perpetual futures on stocks, ETFs, and commodities such as Tesla, Nvidia, gold, and silver, with up to 20x leverage and tokenized shares usable as margin collateral.

- Flux Finance: An overcollateralized lending market governed by the Ondo DAO, where users supply assets like USDC and OUSG to mint interest-bearing fTokens.

- Ondo Bridge: Handles cross-chain minting and burning of USDY using LayerZero, with independent verifiers and rate limiting for security.

Ondo Chain: A Layer 1 for Tokenized Finance

Ondo's most ambitious bet moves beyond issuing tokens to owning the rails they settle on. Ondo Chain is a Layer 1 built specifically for regulated real-world assets, with a testnet live since February 2025 and mainnet targeted for 2026.

The design rests on four pillars: a permissioned validator set of regulated institutions, staking backed by tokenized RWAs rather than only a native token, proof-of-reserve oracles built into the protocol, and native omnichain bridging to public chains. The aim is compliance-by-design, closing the front-running, custody, and reporting gaps that keep large institutions wary of fully public chains.

The trade-off is centralization. Limiting validators to approved entities concentrates control, improving regulatory comfort but stepping back from the open participation that defines most Layer 1s. Ondo's design advisers have included Franklin Templeton and Google Cloud, signaling the institutional audience. With Ondo Global Markets already carrying billions in volume, the chain can launch with real assets and users rather than from zero.

ONDO Tokenomics

The ONDO token launched in January 2024 on Ethereum with a fixed maximum supply of 10 billion. It governs the Ondo DAO and Flux Finance, with voting power proportional to holdings, delegable to other addresses, and active even while tokens are locked.

Allocation and Unlocks

ONDO's supply leans heavily toward long-term ecosystem and development buckets that vest over several years. That schedule dominates near-term supply.

- Ecosystem Growth: ~52.1% for airdrops, contributor incentives, and expansion, much of it on cliff vesting that releases in large scheduled events.

- Protocol Development: ~33% for infrastructure and product building, locked initially and unlocked gradually over several years.

- Private Sales: ~12.9% for seed and Series A investors, subject to lock-ups and incremental release.

- Community Access Sale: ~2% distributed to early supporters through CoinList, most of which unlocked at launch.

A January 18, 2026 unlock released roughly 1.94 billion tokens, worth about $655 million, expanding circulating supply sharply and weighing on price. Around 4.87 billion ONDO, close to half the maximum, circulated by mid-2026, with more unlocks scheduled through 2029.

Utility and the Value-Capture Debate

The central tension in ONDO's design is that the token does not yet capture protocol revenue. Fees from OUSG management, USDY yield spreads, and Global Markets transactions accrue to the business, not holders, decoupling token performance from platform growth.

That gap explains why ONDO traded near $0.32 to $0.40 in mid-2026, far below its December 2024 peak above $2, even as assets under management climbed. The proposed fix is a fee-switch vote planned for the second half of 2026, directing part of an estimated $48 million-plus in annual revenue to holders or buybacks. Whether governance approves it, and how the market prices a TradFi-style infrastructure token, are ONDO's open questions.

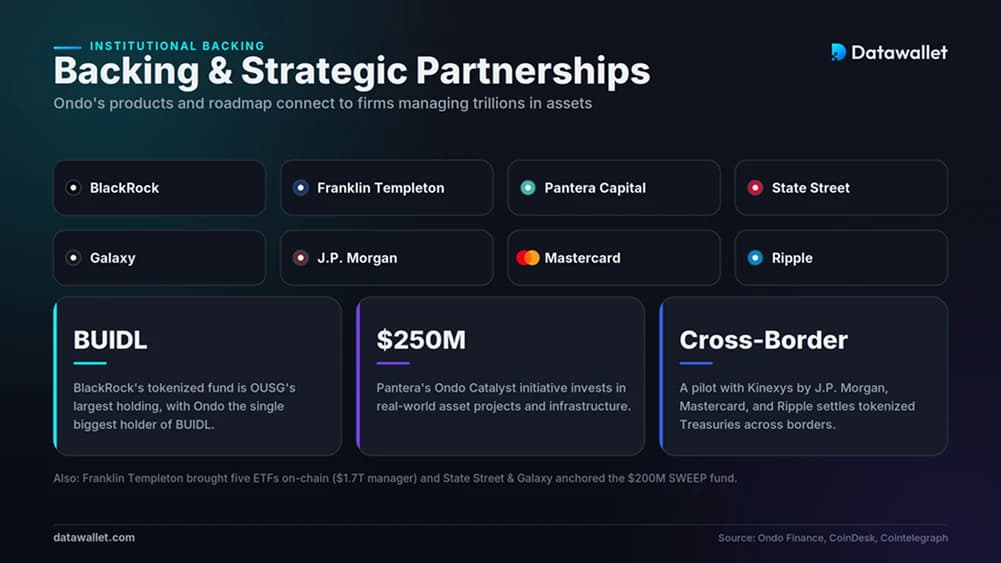

Institutional Backing and Partnerships

Ondo's edge is less about technology than the institutions it has lined up. Its products and roadmap are stitched into firms that manage trillions in traditional assets.

- BlackRock: OUSG's largest underlying holding is BlackRock's BUIDL fund, making Ondo BUIDL's biggest single holder. The relationship is a supply-chain integration rather than a direct equity investment in Ondo.

- Franklin Templeton: In March 2026 the $1.7 trillion manager brought five of its ETFs on-chain through Ondo Global Markets, lending the equity product significant credibility.

- Pantera Capital: Beyond early venture backing, Pantera committed to a $250 million initiative called Ondo Catalyst, focused on RWA projects.

- State Street and Galaxy: The two firms partnered with Ondo on a tokenized liquidity fund called SWEEP, which OUSG is set to anchor with roughly $200 million.

- Cross-Border Settlement: In May 2026 Ondo joined Kinexys by J.P. Morgan, Mastercard, and Ripple on a pilot redeeming tokenized U.S. Treasuries across borders, testing on-chain settlement between major payment rails.

Ondo and the 2026 Regulatory Landscape

Tokenized securities live or die on regulation, and 2026 brought the clarity Ondo had been building toward. The shift turned its compliance-first strategy from a cost into a moat.

The groundwork came through 2025. Ondo registered as an investment advisor, acquired Strangelove for engineering talent, and bought Oasis Pro, gaining an SEC-registered broker-dealer, alternative trading system, and transfer agent license. That package lets it list, settle, and manage tokenized securities inside U.S. rules rather than around them. Late in 2025 the SEC closed a two-year investigation into Ondo without charges, clearing a major overhang.

Policy moved the same way. SEC Chair Paul Atkins has affirmed that tokenized securities are securities under existing law, and the agency approved a Nasdaq rule change in March 2026 letting tokenized versions of listed equities trade under the same tickers and rights as the underlying shares. Pending legislation, including the GENIUS Act for stablecoins and the CLARITY Act splitting oversight between the SEC and CFTC, points toward defined regulatory lanes that favor compliant issuers. For a platform that spent years acquiring licenses, the timing is close to ideal.

How Ondo Compares to Other RWA Platforms

Ondo competes in two markets at once, with different rivals in each. Tokenized Treasuries is concentrated among a few large players, while tokenized equities is a younger contest where Ondo holds a commanding lead.

On the Treasury side, BlackRock's BUIDL fund and Franklin Templeton's BENJI are the heavyweights, backed by managers far larger than Ondo. The relationship is more partnership than rivalry, since OUSG holds BUIDL rather than competing for the same deposits. The broader tokenized asset market has expanded quickly, with tokenized Treasuries alone crossing $10 billion in 2026.

In tokenized equities, Ondo leads. Its 70%-plus issuer-market share reflects a first-mover advantage in a category that barely existed a year earlier, with Securitize and a handful of exchanges still building competing venues. Where most rivals focus on one vertical, Ondo spans Treasuries, equities, derivatives, and its own chain. That breadth is a platform strength, though it also makes the ONDO token a claim on a more complex business than a single-product protocol.

Is Ondo Finance Safe?

Ondo is among the more institutionally credible RWA platforms, with segregated customer assets, third-party reserve attestations, and a full set of U.S. securities licenses. The closed SEC investigation and the bankruptcy-remote structure behind USDY reduce specific failure modes that have plagued less rigorous tokenized products.

Credibility is not zero risk. Ondo's products depend on custodians, fund managers, smart contracts, and a regulatory regime still being written. The ONDO token carries a separate risk profile tied to supply dynamics, not the soundness of the underlying funds.

Risks of Using Ondo

Ondo's assets are conservative by crypto standards, but users should weigh the structural, market, and token-level risks before committing capital.

The main risks include these:

- Custodial Reliance: Every token depends on off-chain custodians, broker-dealers, and funds, so users inherit counterparty exposure beyond the smart contracts.

- Smart Contracts: Minting, redemption, bridging, and lending run on code that audits cannot fully derisk against bugs, oracle failures, or exploits.

- Token Dilution: Scheduled ONDO unlocks through 2029 add supply, and the January 2026 release showed how that pressure can push token price away from platform performance.

- No Direct Fee Accrual: ONDO currently captures no protocol revenue, so its value rests on governance and a fee-switch vote that has not yet passed.

- Regulatory Shifts: Tokenized securities rules are evolving, and changes to eligibility, custody, or trading frameworks could affect product access by jurisdiction.

- Leverage Risk: Ondo Perps introduces up to 20x leverage on volatile equities, where positions can be liquidated quickly during market swings.

- Yield Variability: OUSG and USDY rates float with Treasury yields, so displayed APYs are not fixed and fall when interest rates decline.

The Future of Ondo Finance

Ondo's roadmap pushes deeper into infrastructure. The Ondo Chain mainnet is the headline event, aiming to give institutions a settlement environment built for regulated assets rather than a general-purpose chain retrofitted for them.

Products are expanding in parallel. The June 2026 Ondo Perps launch extends the platform from holding tokenized assets to trading them with leverage, and executives have pointed to tokenized stock TVL reaching several billion dollars by year-end. The SWEEP fund and the cross-border settlement pilot Ondo completed with J.P. Morgan, Mastercard, and Ripple point to a broader ambition: sitting at the center of how tokenized value moves between institutions.

The longer arc depends on adoption and value capture. If Ondo Global Markets scales into the tens of billions and the fee switch sends revenue to ONDO holders, the gap between platform and token could close. If unlocks keep outpacing demand and value capture stays unresolved, the token may keep lagging a business that is otherwise growing fast.

Final Thoughts

Ondo Finance is the clearest example of regulated tokenization at scale. It pairs conservative, fully-backed Treasury and equity products with a licensing stack and institutional partnerships few crypto-native firms can match, and the numbers, from $3.5 billion in assets to a 70%-plus equity market share, back the positioning.

The harder question sits with the ONDO token, not the platform. Strong product growth has not translated into token performance, because ONDO governs the protocol without yet sharing its revenue. The planned fee-switch vote is the pivot worth watching.

For anyone tracking the RWA narrative, Ondo is a serious contender and arguably the category leader. Whether that becomes token value depends on governance, the pace of unlocks, and how the market learns to price tokenized-finance infrastructure over the coming year.