Stablecoin Statistics & Trends for 2026

The stablecoin market reached roughly $320 billion in June 2026, with USDT and USDC controlling more than $263 billion combined. Daily volume, chain distribution and issuer concentration show how much liquidity still depends on a few dollar-pegged tokens.

Stablecoins also anchor DeFi activity, with Ethereum alone holding about $160.95 billion in stablecoin supply. Perp DEXs processed more than $579 billion in 30-day volume, while lending yields mostly compressed into the 2%-6% range.

The market is expanding beyond plain dollar tokens. Challenger issuers now represent about $56.1 billion, tokenized commodities reached $5.55 billion, and Citi’s base case projects stablecoins could reach $1.9 trillion by 2030.

Top 8 Stablecoin Statistics and Trends

1. Stablecoin Market Capitalization Hit $319.9 Billion in June

Stablecoin capitalization is hovering just under its April high. DefiLlama showed $319.9 billion on June 1, with USDT dominance at 58.74%, while CoinGecko showed $315.0 billion and $89.5 billion in 24-hour stablecoin trading volume. The gap reflects different inclusion rules and update windows across trackers.

The market is no longer in explosive expansion mode, but it is still materially larger than early 2025. The Federal Reserve noted stablecoins reached $317 billion by April 6, 2026, up more than 50% since early 2025, with DeFi usage and transaction volumes also surging.

2. USDT and USDC Still Control $263.8 Billion

The leaderboard remains concentrated, but the second tier is changing faster as USDS, USD1, DAI, USDe, PYUSD, BUIDL and USYC compete for institutional liquidity.

Current Top Stablecoins by June Market Capitalization Snapshot:

- USDT: DefiLlama lists Tether at $187.9 billion, giving it 58.74% market dominance and keeping it the default liquidity asset across centralized exchanges and Tron flows.

- USDC: Circle’s USDC sits at $75.9 billion on DefiLlama, with CoinGecko showing $15.1 billion in daily volume and strong Ethereum, Solana, Base, and Hyperliquid utility.

- USDS: Sky Dollar ranks third on DefiLlama at $8.82 billion, reflecting MakerDAO’s rebrand and continued demand for savings-rate-linked dollar liquidity inside DeFi credit markets today.

- USD1: World Liberty Financial USD reached $4.74 billion, moving ahead of DAI on DefiLlama and showing how politically branded issuers can scale quickly when exchange distribution improves.

- DAI: Dai remains near $4.58 billion, but it now trails newer or rebranded rivals as Sky increasingly pushes users toward USDS and sUSDS products instead.

- USDe: Ethena USDe stands near $4.5 billion, rebounding 15.36% over one month on DefiLlama after CoinDesk reported a 36.1% April contraction from Aave unwind pressure.

3. Perp DEXs Processed $579.2 Billion in 30 Days

Perpetual futures are one of stablecoins’ highest-velocity uses. DefiLlama’s live perp dashboard showed $16.1 billion in 24-hour DEX perp volume and $579.2 billion over 30 days, while CoinGecko’s May report put top perp DEX monthly volume at $611.6 billion in 2026 across the leading protocols tracked.

Stablecoins are the working collateral behind that leverage. Hyperliquid documents USDC margining for its USDT-denominated linear contracts, Circle says USDC remains Hyperliquid’s primary collateral, and Binance’s USDⓈ-M futures are quoted and settled in USDT or USDC, which keeps trader PnL dollar-based instead of coin-based risk.

4. DeFi Stablecoins Anchor $160.9 Billion on Ethereum

Inside DeFi, stablecoins function less like idle cash and more like balance-sheet inventory. DefiLlama shows $160.95 billion of stablecoins on Ethereum alone, with USDT holding 50.33% of that chain’s stablecoin base and stablecoins roughly matching DeFi TVL across core application chains as collateral liquidity today.

The Aave stress test made that role visible. Coin Metrics coverage reported stablecoin pools as Aave’s primary liquidity reservoir, with over $2 billion withdrawn within 24 hours and USDT, USDC and USDe markets pushed to 100% utilization during the April KelpDAO contagion event liquidity shock.

5. Stablecoin Yields Cluster Around 2% to 6%

Stablecoin yields are not as high as they used to be. Most sustainable rates now come from borrower demand, savings-rate products, fixed-rate markets, or RWA-linked cashflows, not incentives.

Current Yield Benchmarks From Recent Dashboards and Research:

- Aave USDC: DefiLlama shows USDC on Aave V3 Ethereum at 3.24% APY, with a 3.80% 30-day average and $184.35 million TVL for the pool snapshot today.

- Aave Umbrella: Aave’s USDC Umbrella pool shows 7.41% APY on DefiLlama, but with smaller $53.44 million TVL and higher product-specific risk than plain lending markets today.

- Sky sUSDS: DefiLlama lists sUSDS on Sky Lending Arbitrum at 3.60% APY, 3.65% 30-day average, and $358.79 million TVL as a savings-rate benchmark route today.

- Morpho USDT: DefiLlama’s BBQUSDT Morpho Blue pool shows 4.80% APY and 5.10% 30-day average, illustrating higher curated-vault rates with curator risk and smaller pool depth today.

- Ethena sUSDe: CoinDesk reported Ethena’s sUSDe APY compressed to about 3.5%, after earlier incentive-heavy yields above 40% pulled billions into the product during 2024-2025 demand cycle.

- Stress Rates: Coin Metrics coverage reported April stress briefly pushed USDT and USDC supply APYs near 13%, while DAI exceeded 24% before liquidity normalized across pools.

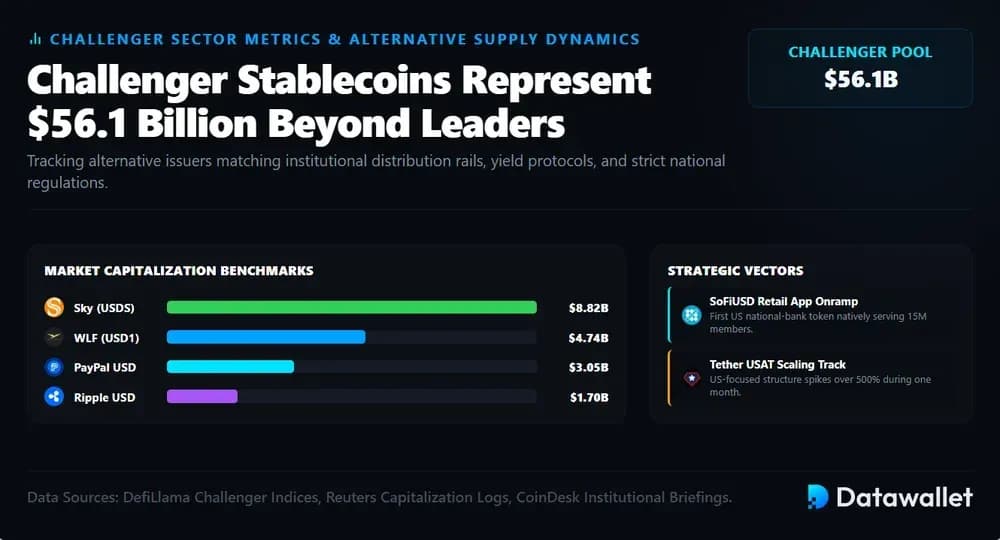

6. Challenger Stablecoins Now Represent $56.1 Billion Beyond Leaders

The top two still dominate, but the non-USDT, non-USDC pool now equals about $56.1 billion, creating room for issuers with distribution, yield, or regulation.

Current Challenger Stablecoin Market Cap Snapshot Beyond Leaders:

- USDS: At $8.82 billion, USDS leads the challenger group and benefits from Sky’s migration away from DAI plus its savings-rate product ecosystem in DeFi markets.

- USD1: DefiLlama puts USD1 at $4.74 billion, and Reuters said it was already the fifth-largest stablecoin by market capitalization after a February peg attack event.

- PYUSD: PayPal USD sits near $3.05 billion on DefiLlama, while PayPal expanded PYUSD access to 70 additional markets in March 2026 to widen adoption globally.

- RLUSD: Ripple USD reached $1.70 billion on DefiLlama; CoinDesk reported it surpassed $1 billion less than a year after its 2024 launch on institutional demand.

- SoFiUSD: CoinDesk reported SoFiUSD launched to nearly 15 million members, becoming the first US national-bank stablecoin offered directly through a retail app on public blockchains.

- USAT: CoinDesk reported Tether’s US-focused stablecoin grew over 500% in one month, though it still trails USDT and major regulated rivals at early scale today.

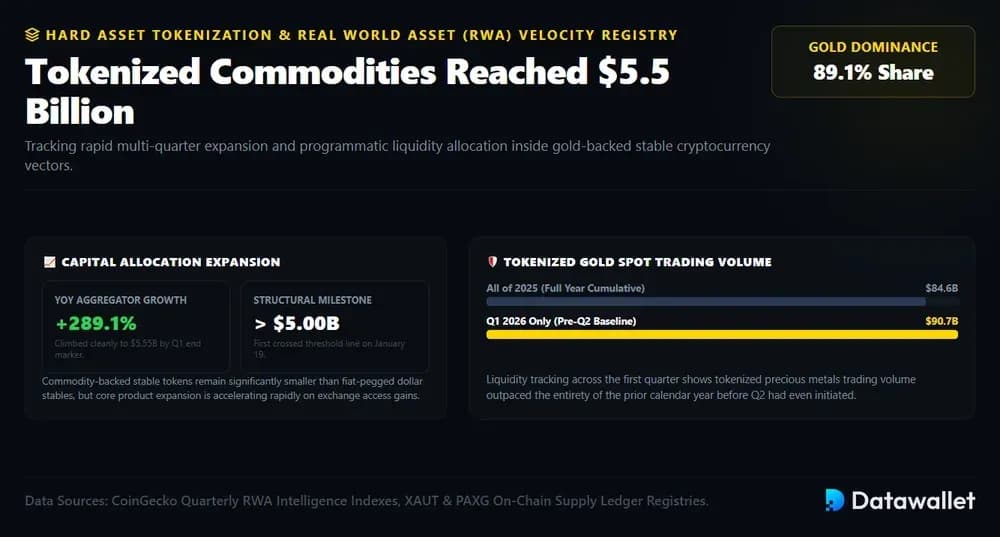

7. Tokenized Commodities Reached $5.5 Billion, Mostly Gold

Commodity-backed stablecoins are still small versus dollar stables, but growth is unusually fast. CoinGecko’s May 2026 RWA report says tokenized commodities climbed 289.1% to $5.55 billion by Q1 end, after first crossing $5 billion on January 19 as gold rallied and exchange access improved materially.

Gold-backed stable cryptocurrencies are the branch that matters. XAUT and PAXG accounted for 89.1% of commodity-token expansion, while tokenized gold spot volume hit $90.7 billion in Q1 2026, already beating the $84.6 billion traded through all of 2025 before the second quarter even started for crypto investors.

8. Citi Sees Stablecoins Reaching $1.9 Trillion by 2030

Forecasts now assume stablecoins become core tokenization infrastructure. Citi’s September 2025 Stablecoins 2030 report raised its issuance forecast to $1.9 trillion in the base case and $4.0 trillion in the bull case, citing faster growth and a wider project pipeline globally by 2030 across markets.

RWA data shows why stablecoins will likely remain the dominant on-chain real-world asset for now. RWA.xyz lists $26.71 billion in distributed asset value versus $299.30 billion in total stablecoin value, while CoinGecko found RWAs were only 6.4% of stablecoins at Q1 end despite triple-digit tokenization growth.

How Are Stablecoins Regulated?

Stablecoin regulation centers on licensing, reserve quality, redemption rights, custody, payments use and anti-money-laundering controls. The strictest regimes treat fiat-backed stablecoins like payment instruments, not speculative crypto assets.

1. United States

In the United States, the Office of the Comptroller of the Currency is implementing GENIUS Act rules for payment stablecoin issuance. The law generally prohibits anyone other than a permitted payment stablecoin issuer from issuing payment stablecoins in the US

The proposed framework separates payment stablecoins from investment products, while creating federal oversight for qualified issuers. It also covers reserve composition, redemption timing, custody, capital, risk management and reporting, with additional AML and sanctions rules expected through Treasury coordination.

2. United Kingdom

In the United Kingdom, the Financial Conduct Authority is designing rules for qualifying stablecoin issuance and cryptoasset custody. The FCA’s approach treats qualifying stablecoins as money-like instruments rather than investment products, with authorization and conduct standards for issuers.

The Bank of England will supervise systemic sterling-denominated stablecoins used for UK payments. Its consultation focuses on non-bank issuers, backing assets, redemption, potential holding limits and systemic payment risks.

3. European Union

In the European Union, the European Securities and Markets Authority coordinates MiCA rules for crypto-asset markets. MiCA creates uniform EU rules for issuers and service providers, including transparency, disclosure, authorization and supervision requirements for asset-referenced and e-money tokens.

The European Banking Authority handles technical standards and supervisory work for stablecoin-like tokens. Under MiCA, asset-referenced tokens and e-money tokens face reserve, redemption, governance and authorization rules, with stricter treatment for significant issuers.

4. Asia

Asia has the broadest regulatory spread: Singapore, Hong Kong and Japan already have dedicated regimes, while South Korea, Taiwan and Thailand are still refining models around payments, reserves and monetary sovereignty.

Key Asian regulatory approaches include:

- Singapore: The Monetary Authority of Singapore finalized a single-currency stablecoin framework covering Singapore-issued tokens pegged to SGD or G10 currencies, with reserve, redemption, capital and disclosure requirements.

- Hong Kong: The Hong Kong Monetary Authority supervises fiat-referenced stablecoin issuers under the Stablecoins Ordinance, which made issuance a licensed activity from August 1, 2025.

- Japan: The Financial Services Agency treats stablecoins as electronic payment instruments, with licensed issuers and intermediaries subject to transfer-notification, AML and consumer-protection rules.

- South Korea: The Bank of Korea has not opposed won-based stablecoins outright, but remains concerned about capital flows, foreign-exchange pressure and non-bank issuance.

- China: The People’s Bank of China maintains a prohibition-focused stance, saying virtual currencies, including stablecoins, lack legal-tender status and remain linked to illegal financial activity risks.

- Thailand: The Bank of Thailand keeps baht-pegged stablecoins tightly controlled, while non-baht stablecoins may be treated through existing digital-asset listing and exchange rules.

- Taiwan: The Financial Supervisory Commission has proposed a Virtual Asset Services Act that defines fiat-pegged stablecoins as virtual assets requiring formal supervision.

- United Arab Emirates: The Central Bank of the UAE regulates payment-token services and restricts payment use to approved dirham or licensed foreign-currency stablecoins.

5. Rest of The World

Outside the largest crypto hubs, regulators are moving from general VASP rules toward stablecoin-specific reserve, redemption and payment frameworks, especially where dollar stablecoins are already used for cross-border transfers.

Notable non-Asian regulatory approaches include:

- Canada: The Department of Finance Canada proposed a federal fiat-backed stablecoin framework focused on reserves, par redemption, governance and Bank of Canada oversight.

- Brazil: The Central Bank of Brazil tightened virtual-asset rules, classifying fiat-pegged virtual-asset payments and transfers as foreign-exchange operations subject to authorization, transparency and AML controls.

- Australia: The Australian Securities and Investments Commission finalized stablecoin and wrapped-token relief, while broader payments reforms are expected to capture payment stablecoin products.

- South Africa: The South African Reserve Bank is assessing crypto assets used for domestic payments after crypto assets were classified as financial products under South African financial-services law.

- Switzerland: The Swiss Financial Market Supervisory Authority clarified stablecoin treatment through guidance focused on bank guarantees, AML risks and issuer obligations for fiat-referenced tokens.

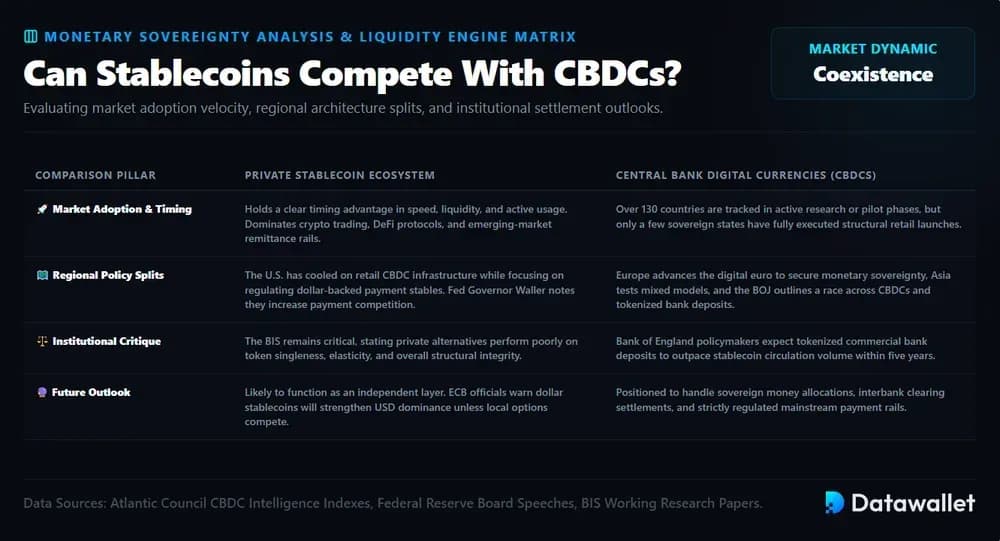

Can Stablecoins Compete With CBDCs?

Stablecoins already compete with CBDCs in speed, liquidity and market adoption, especially because most countries are still researching or piloting CBDCs. The Atlantic Council CBDC Tracker follows 130+ countries, but only a few have fully launched retail CBDCs, leaving private stablecoins with a timing advantage.

The regional split is sharp. The US has cooled on a retail CBDC while regulating dollar stablecoins, Europe is advancing the digital euro for monetary sovereignty, and Asia is testing mixed models. Bank of Japan officials describe this as a broader race among CBDCs, stablecoins and tokenized deposits.

Opinions differ on who wins. Fed Governor Christopher Waller has argued stablecoins can improve payments and increase competition, while Bank of England policymaker Megan Greene expects tokenized bank deposits to overtake stablecoins within five years. The BIS remains more skeptical, saying stablecoins perform poorly on singleness, elasticity and integrity.

The likely outcome is coexistence, not replacement. Stablecoins may dominate crypto trading, DeFi, dollar payments and emerging-market remittances, while CBDCs and tokenized deposits handle sovereign money, bank settlement and regulated payment rails. ECB officials warn dollar stablecoins could strengthen dollar dominance unless local digital money becomes competitive.

Is There a Future For Decentralized Stablecoins?

Decentralized stablecoins still have a future, but the category carries heavy baggage. Earlier designs showed that weak collateral, reflexive incentives and governance flaws can destroy dollar pegs quickly, especially during liquidity stress or market-wide deleveraging.

Major failures shaped today’s stablecoin design:

- TerraUSD: UST collapsed in May 2022 after losing its dollar peg, exposing the weakness of algorithmic backing tied to LUNA demand.

- Iron Finance: IRON and TITAN suffered a DeFi bank run in 2021, showing how partial collateralization can spiral when confidence breaks.

- Beanstalk: The protocol lost more than $180 million after a governance attack used borrowed voting power to drain reserves.

- DEI: Deus Finance’s DEI dropped as low as $0.54, becoming another algorithmic stablecoin hit by the post-Terra confidence shock.

The current market has shifted toward collateralized, yield-linked and risk-managed designs. DefiLlama lists USDS, DAI, USDe and GHO among the largest non-fiat-issued alternatives, but their models differ sharply: overcollateralized lending, protocol savings rates, delta-neutral hedging and DeFi-native minting.

The largest survivor is MakerDAO’s successor ecosystem. Sky’s USDS is backed by surplus collateral and peg-stability modules, while DAI remains in circulation. That model is less “purely decentralized” than early crypto ideals, but it has proven more durable than reflexive algorithmic pegs.

Newer designs are trying to reduce dependence on a single collateral type. Ethena’s USDe uses automated delta-neutral hedges, while Aave’s GHO links issuance to lending markets and governance controls. The future likely belongs to hybrid decentralized stablecoins that prioritize collateral transparency, liquid backing and conservative risk parameters.

What are the Risks of Stablecoins?

Stablecoins reduce crypto volatility, but they still carry issuer, reserve, liquidity, regulatory and systemic risks that can affect users, markets and payment flows.

The main stablecoin risk categories include:

- Peg Risk: Stablecoins can trade below $1 when confidence breaks, liquidity thins or collateral becomes uncertain, as TerraUSD showed during its May 2022 collapse.

- Reserve Risk: Issuers may hold reserves in assets that are less liquid, less transparent or harder to sell quickly than users assume during redemption pressure.

- Run Risk: Large redemption waves can force issuers to liquidate reserve assets quickly, potentially creating fire-sale pressure in Treasury, repo or money-market instruments.

- Issuer Risk: Users depend on the issuer’s governance, audits, custody partners, banking access and redemption operations, even when the token itself moves on-chain.

- Regulatory Risk: The FSB says global stablecoin rules remain inconsistent across jurisdictions, creating uncertainty for issuers, exchanges, payment firms and cross-border users.

- Illicit Finance Risk: Permissionless stablecoins can be moved through pseudonymous wallets, mixers, cross-chain bridges or offshore platforms, making AML and sanctions controls harder.

- Monetary Risk: Dollar stablecoins can increase dependence on US dollar liquidity abroad, weakening local monetary control and raising currency-substitution risks in emerging markets.

- DeFi Risk: Stablecoins used in lending, bridges and derivatives inherit smart contract, oracle, liquidation and composability risks, especially when protocols reuse the same collateral base.

Final Thoughts

Stablecoins are the core of crypto liquidity, with hundreds of billions in circulating supply across exchanges, DeFi, payments and tokenized assets. Their next growth phase depends on stronger regulation, deeper distribution and clearer reserve standards.

Through 2026, the market will reward issuers with transparent backing, reliable redemption, broad exchange support and credible oversight. Weak collateral, opaque audits or uncertain licensing could limit adoption, especially as banks launch competing digital money products.

Users should treat stablecoins as financial products with issuer, reserve and protocol risk. Peg history, custody structure, jurisdiction, collateral quality and DeFi exposure matter before holding large balances or using stablecoins for yield.

Our Methodology

This article combines live stablecoin dashboards, market capitalization trackers, yield databases, RWA datasets, central bank publications, regulator materials and institutional research to evaluate stablecoin statistics, trends, regulation and risks in 2026.

How The Data Was Compiled:

- Market Trackers: Used DefiLlama and CoinGecko for stablecoin market capitalization, issuer rankings, chain distribution, trading volume, dominance, supply changes and category-level comparisons.

- Yield Dashboards: Used DefiLlama yield data for stablecoin lending rates, savings products, DeFi pools, 30-day averages, TVL and protocol-specific APY comparisons.

- DeFi Data: Reviewed perp DEX dashboards, lending market data and stablecoin chain flows to assess how USDT, USDC, USDS, DAI and USDe are used across DeFi.

- RWA Research: Used CoinGecko, RWA.xyz and issuer-level data to evaluate tokenized commodities, gold-backed stablecoins, real-world asset growth and stablecoin dominance within tokenized finance.

- Regulatory Sources: Reviewed materials from the OCC, FCA, Bank of England, ESMA, EBA, MAS, HKMA, FSA, FINMA and other regulators for jurisdiction-specific stablecoin rules.

- Central Bank Research: Used publications from the Federal Reserve, BIS, ECB and other central banks to compare stablecoins with CBDCs, tokenized deposits and payment-system policy.

- News Reporting: Referenced high-credibility outlets such as Reuters, CoinDesk and official press releases for recent launches, enforcement updates, policy changes and market incidents.

- Risk Review: Compared historical depegs, reserve failures, governance attacks, redemption stress and DeFi contagion events to explain the main risks users face today.

- Snapshot Caveat: Many figures come from live dashboards, so values can change as supply shifts, issuers mint or redeem tokens, yields update and market liquidity rotates.

Frequently asked questions

.webp)